options(conflicts.policy = "depends.ok")

devtools::source_url("https://github.com/jjcurtin/lab_support/blob/main/fun_ml.R?raw=true")ℹ SHA-1 hash of file is "77e91675366f10788c6bcb59fa1cfc9ee0c75281"tidymodels_conflictRules()Use of root mean square error (RMSE) in training and validation sets for model performance evaluation

The General Linear Model as a machine learning model

K Nearest Neighbor (KNN)

Post questions to the Readings channel in Slack

Post questions to the video-lectures channel in Slack

Post questions to the application-assignments channel in Slack

Submit the application assignment here and complete the unit quiz by 8 pm on Wednesday, February 7th

Our goal in this unit is to build a machine learning regression model that can accurately (we hope) predict the sale_price for future sales of houses (in Iowa? more generally?)

To begin this project we need to:

options(conflicts.policy = "depends.ok")

devtools::source_url("https://github.com/jjcurtin/lab_support/blob/main/fun_ml.R?raw=true")ℹ SHA-1 hash of file is "77e91675366f10788c6bcb59fa1cfc9ee0c75281"tidymodels_conflictRules()tidymodels and tidyverse because the other functions we need are only called occasionally (so we will call them by namespace to see how that “feels”.)library(tidyverse) # for general data wrangling

library(tidymodels) # for modelingdevtools::source_url("https://github.com/jjcurtin/lab_support/blob/main/fun_eda.R?raw=true")ℹ SHA-1 hash of file is "c045eee2655a18dc85e715b78182f176327358a7"devtools::source_url("https://github.com/jjcurtin/lab_support/blob/main/fun_plots.R?raw=true")ℹ SHA-1 hash of file is "def6ce26ed7b2493931fde811adff9287ee8d874"theme_set(theme_classic())

options(tibble.width = Inf)path_data <- "./data"class_ames <- function(df){

df |>

mutate(across(where(is.character), factor)) |>

mutate(overall_qual = factor(overall_qual, levels = 1:10),

1 garage_qual = suppressWarnings(fct_relevel(garage_qual,

c("no_garage", "po", "fa",

"ta", "gd", "ex"))))

}suppressWarnings()

data_trn <-

read_csv(here::here(path_data, "ames_clean_class_trn.csv"),

col_types = cols()) |>

class_ames() |>

glimpse()Rows: 1,465

Columns: 10

$ sale_price <dbl> 105000, 126000, 115000, 120000, 99500, 112000, 122000, 12…

$ gr_liv_area <dbl> 896, 882, 864, 836, 918, 1902, 900, 1225, 1728, 858, 1306…

$ lot_area <dbl> 11622, 8400, 10500, 2280, 7892, 8930, 9819, 9320, 13260, …

$ year_built <dbl> 1961, 1970, 1971, 1975, 1979, 1978, 1967, 1959, 1962, 195…

$ overall_qual <fct> 5, 4, 4, 7, 6, 6, 5, 4, 5, 5, 3, 5, 4, 5, 3, 5, 2, 6, 5, …

$ garage_cars <dbl> 1, 2, 0, 1, 1, 2, 1, 0, 0, 0, 0, 1, 2, 2, 1, 1, 2, 2, 1, …

$ garage_qual <fct> ta, ta, no_garage, ta, ta, ta, ta, no_garage, no_garage, …

$ ms_zoning <fct> res_high, res_low, res_low, res_low, res_low, res_med, re…

$ lot_config <fct> inside, corner, fr2, fr2, inside, inside, inside, inside,…

$ bldg_type <fct> one_fam, one_fam, one_fam, town_inside, town_end, duplex,…data_val <- read_csv(here::here(path_data, "ames_clean_class_val.csv"),

col_types = cols()) |>

class_ames() |>

glimpse()Rows: 490

Columns: 10

$ sale_price <dbl> 215000, 189900, 189000, 171500, 212000, 164000, 394432, 1…

$ gr_liv_area <dbl> 1656, 1629, 1804, 1341, 1502, 1752, 1856, 1004, 1092, 106…

$ lot_area <dbl> 31770, 13830, 7500, 10176, 6820, 12134, 11394, 11241, 168…

$ year_built <dbl> 1960, 1997, 1999, 1990, 1985, 1988, 2010, 1970, 1971, 197…

$ overall_qual <fct> 6, 5, 7, 7, 8, 8, 9, 6, 5, 6, 7, 9, 8, 8, 7, 8, 6, 5, 5, …

$ garage_cars <dbl> 2, 2, 2, 2, 2, 2, 3, 2, 1, 2, 2, 2, 2, 3, 2, 3, 1, 1, 2, …

$ garage_qual <fct> ta, ta, ta, ta, ta, ta, ta, ta, ta, ta, ta, ta, ta, ta, t…

$ ms_zoning <fct> res_low, res_low, res_low, res_low, res_low, res_low, res…

$ lot_config <fct> corner, inside, inside, inside, corner, inside, corner, c…

$ bldg_type <fct> one_fam, one_fam, one_fam, one_fam, town_end, one_fam, on…NOTE: Remember, I have held back an additional test set that we will use only once to evaluate the final model that we each develop in this unit.

We will also make a dataframe to track validation error across the models we fit

error_val <- tibble(model = character(), rmse_val = numeric()) |>

glimpse()Rows: 0

Columns: 2

$ model <chr>

$ rmse_val <dbl> We will fit regression models with various model configurations.

These configurations will differ with respect to statistical algorithm:

These configurations will differ with respect to the features

To build models that will work well in new data (e.g., the data that I have held back from you so far):

We have split the remaining data into a training and validation set for our own use during model building

We will fit models in train

We will evaluate them in validation

Remember that we:

sale_price) split of the data at the end of cleaning EDA to create training and validation setsYou will work with all of my predictors and all the predictors you used for your EDA when you do the application assignment for this unit

Pause for a moment to answer this question:

Let’s take a quick look at the available raw predictors in the training set

data_trn |> skim_all()| Name | data_trn |

| Number of rows | 1465 |

| Number of columns | 10 |

| _______________________ | |

| Column type frequency: | |

| factor | 5 |

| numeric | 5 |

| ________________________ | |

| Group variables | None |

Variable type: factor

| skim_variable | n_missing | complete_rate | n_unique | top_counts |

|---|---|---|---|---|

| overall_qual | 0 | 1 | 10 | 5: 424, 6: 350, 7: 304, 8: 176 |

| garage_qual | 0 | 1 | 5 | ta: 1312, no_: 81, fa: 57, gd: 13 |

| ms_zoning | 0 | 1 | 7 | res: 1157, res: 217, flo: 66, com: 13 |

| lot_config | 0 | 1 | 5 | ins: 1095, cor: 248, cul: 81, fr2: 39 |

| bldg_type | 0 | 1 | 5 | one: 1216, tow: 108, dup: 63, tow: 46 |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789 | 129500 | 160000 | 213500 | 745000 | 1.64 | 4.60 |

| gr_liv_area | 0 | 1 | 1506.84 | 511.44 | 438 | 1128 | 1450 | 1759 | 5642 | 1.43 | 5.19 |

| lot_area | 0 | 1 | 10144.16 | 8177.55 | 1476 | 7500 | 9375 | 11362 | 164660 | 11.20 | 182.91 |

| year_built | 0 | 1 | 1971.35 | 29.65 | 1880 | 1953 | 1972 | 2000 | 2010 | -0.54 | -0.62 |

| garage_cars | 1 | 1 | 1.78 | 0.76 | 0 | 1 | 2 | 2 | 4 | -0.26 | 0.10 |

Remember from our modeling EDA that we have some issues to address as part of our feature engineering:

sale_priceAll of this will be accomplished with a recipe

But first, let’s discuss/review our first statistical algorithm

We will start with only a quick review of the use of the simple (one feature) linear model (LM) as a machine learning model because you should be very familiar with this statistical model at this point

Applied to our regression problem, we might fit a model such as:

The (general) linear model is a parametric model. We need to estimate two parameters using our training set

You already know how to do this using lm() in base R. However, we will use the tidymodels modeling approach.

We use tidymodels because:

To fit a model with a specific configuration, we need to:

prep() it with training databake() it with data you want to use to calculate feature matrixThese steps are accomplished with functions from the recipes and parsnip packages.

We will start with a simple model configuration

gr_liv_area)Set up a VERY SIMPLE feature engineering recipe

~~.rec <-

recipe(sale_price ~ gr_liv_area, data = data_trn) recsummary(rec)We can then prep the recipe and bake the data to make our feature matrix from the training dataset

data_trn and then bake data_trn so that we have features from our training set to train/fit the model.rec_prep <- rec |>

prep(training = data_trn)new_data = NULLfeat_trn <- rec_prep |>

bake(new_data = NULL)You should always review the feature matrix to make sure it looks as you expect

sale_price)gr_liv_area)feat_trn |> skim_all()| Name | feat_trn |

| Number of rows | 1465 |

| Number of columns | 2 |

| _______________________ | |

| Column type frequency: | |

| numeric | 2 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1506.84 | 511.44 | 438 | 1128 | 1450 | 1759 | 5642 | 1.43 | 5.19 |

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789 | 129500 | 160000 | 213500 | 745000 | 1.64 | 4.60 |

Now let’s consider the statistical algorithm

tidymodels breaks this apart into two pieces for claritylinear_reg(), nearest_neighbor(), logistic_reg()set_mode() to indicate if if the model is for regression or classification broadly

'linear_reg() is only for regression.tidymodels calls this setting the enginelm, kknn, glm, glmnetYou can see the available engines (and modes: regression vs. classification) for the broad classes of algorithms

We will work with many of these algorithms later in the course

show_engines("linear_reg")# A tibble: 7 × 2

engine mode

<chr> <chr>

1 lm regression

2 glm regression

3 glmnet regression

4 stan regression

5 spark regression

6 keras regression

7 brulee regressionshow_engines("nearest_neighbor")# A tibble: 2 × 2

engine mode

<chr> <chr>

1 kknn classification

2 kknn regression show_engines("logistic_reg")# A tibble: 7 × 2

engine mode

<chr> <chr>

1 glm classification

2 glmnet classification

3 LiblineaR classification

4 spark classification

5 keras classification

6 stan classification

7 brulee classificationshow_engines("decision_tree")# A tibble: 5 × 2

engine mode

<chr> <chr>

1 rpart classification

2 rpart regression

3 C5.0 classification

4 spark classification

5 spark regression show_engines("rand_forest")# A tibble: 6 × 2

engine mode

<chr> <chr>

1 ranger classification

2 ranger regression

3 randomForest classification

4 randomForest regression

5 spark classification

6 spark regression show_engines("mlp")# A tibble: 6 × 2

engine mode

<chr> <chr>

1 keras classification

2 keras regression

3 nnet classification

4 nnet regression

5 brulee classification

6 brulee regression You can load even more engines from the discrim package. We will use some of these later too. You need to load the package to use these engines.

library(discrim, exclude = "smoothness") # needed for these engines

show_engines("discrim_linear") # A tibble: 4 × 2

engine mode

<chr> <chr>

1 MASS classification

2 mda classification

3 sda classification

4 sparsediscrim classificationshow_engines("discrim_regularized") # A tibble: 1 × 2

engine mode

<chr> <chr>

1 klaR classificationshow_engines("naive_Bayes")# A tibble: 2 × 2

engine mode

<chr> <chr>

1 klaR classification

2 naivebayes classificationYou can also better understand how the engine will be called using translate()

Not useful here but will be with more complicated algorithms

linear_reg() |>

set_engine("lm") |>

translate()Linear Regression Model Specification (regression)

Computational engine: lm

Model fit template:

stats::lm(formula = missing_arg(), data = missing_arg(), weights = missing_arg())Let’s combine our feature matrix with an algorithm to fit a model in our training set using only raw gr_liv_area as a feature

Note the specification of

lm are only for the regression mode). to indicate all features in the matrix.

gr_liv_area. for all features and use of feature matrix from training set

We can get the parameter estimates, standard errors, and statistical tests for each \(\beta\) = 0 for this model using tidy() from the broom package (loaded as part of the tidyverse)

fit_lm_1 |> tidy()# A tibble: 2 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 16561. 4537. 3.65 2.72e- 4

2 gr_liv_area 109. 2.85 38.2 4.78e-222There are a variety of ways to pull out the estimates for each feature (and intercept)

Option 1: Pull all estimates from the tidy object

fit_lm_1 |>

tidy() |>

pull(estimate)[1] 16560.9991 108.9268Option 2: Extract a single estimate using $ and row number. Be careful that order of features won’t change! This assumes the feature coefficient for the relevant feature is always the second coefficient.

tidy(fit_lm_1)$estimate[[2]][1] 108.9268Option 3: Filter tidy df to the relevant row (using term ==) and pull the estimate. Safer!

fit_lm_1 |>

tidy() |>

filter(term == "gr_liv_area") |>

pull(estimate)[1] 108.9268Option 4: Write a function if we plan to do this a lot. We include this function in the fun_ml.R script in our repo. Better still (safe and code efficient)!

get_estimate <- function(the_fit, the_term){

the_fit |>

tidy() |>

filter(term == the_term) |>

pull(estimate)

}and then use this function

get_estimate(fit_lm_1, "gr_liv_area")[1] 108.9268get_estimate(fit_lm_1, "(Intercept)")[1] 16561Regardless of the method, we now have a simple parametric model for sale_price

\(\hat{sale\_price} = 1.6561\times 10^{4} + 108.9 * gr\_liv\_area\)

We can get the predicted values for sale_price (i.e., \(\hat{sale\_price}\)) in our validation set using predict()

However, we first need to make a feature matrix for our validation set

data_trn)data_valfeat_val <- rec_prep |>

bake(new_data = data_val)As always, we should skim these new features

feat_val |> skim_all()| Name | feat_val |

| Number of rows | 490 |

| Number of columns | 2 |

| _______________________ | |

| Column type frequency: | |

| numeric | 2 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1493.0 | 483.78 | 480 | 1143.5 | 1436 | 1729.5 | 3608 | 0.92 | 1.16 |

| sale_price | 0 | 1 | 178512.8 | 75493.59 | 35311 | 129125.0 | 160000 | 213000.0 | 556581 | 1.42 | 2.97 |

Now we can get predictions using our model with validation features

predict() returns a dataframe with one column named .pred and one row for every observation in dataframe (e.g., validation feature set)

predict(fit_lm_1, feat_val)# A tibble: 490 × 1

.pred

<dbl>

1 196944.

2 194003.

3 213065.

4 162632.

5 180169.

6 207401.

7 218729.

8 125923.

9 135509.

10 133004.

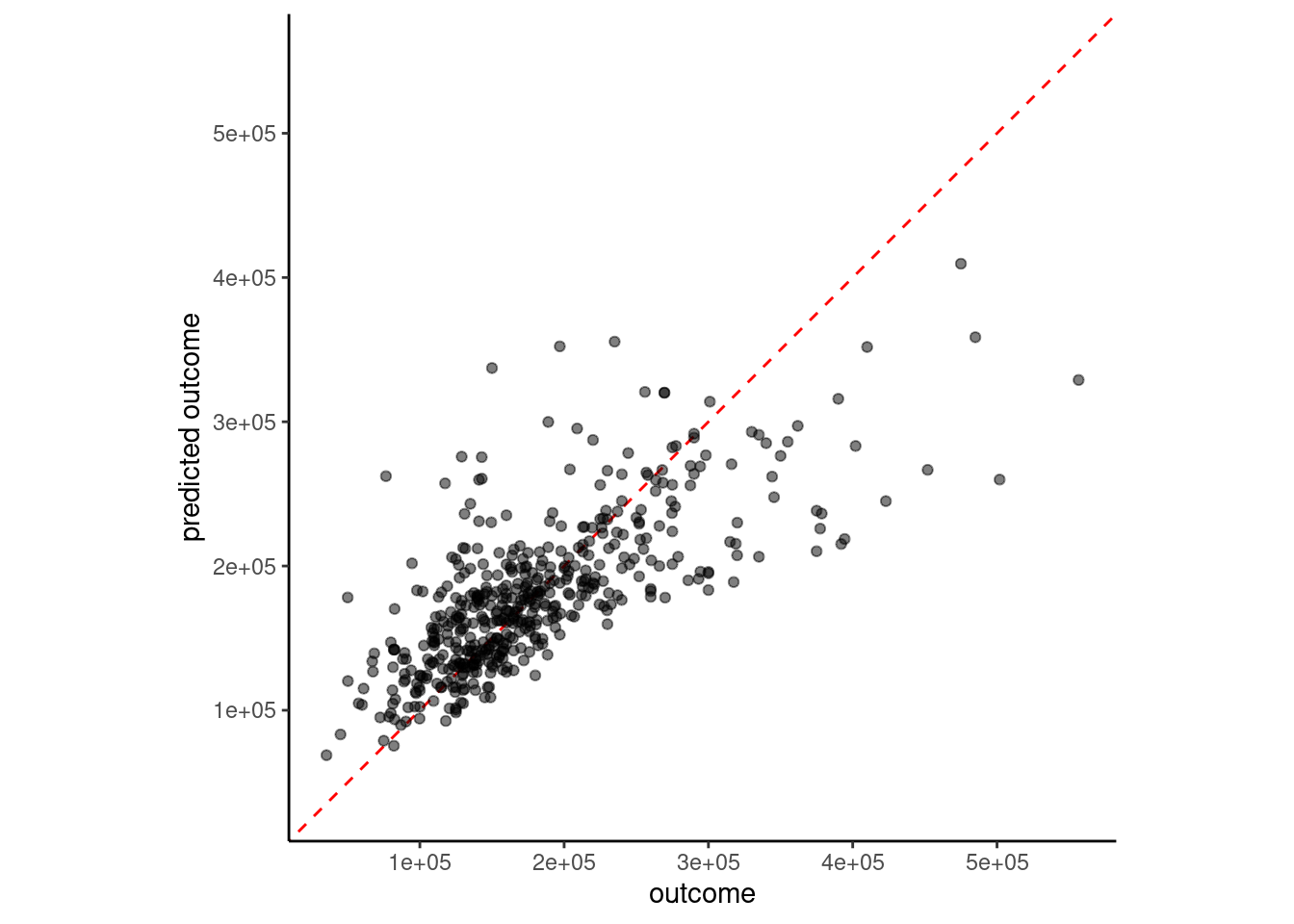

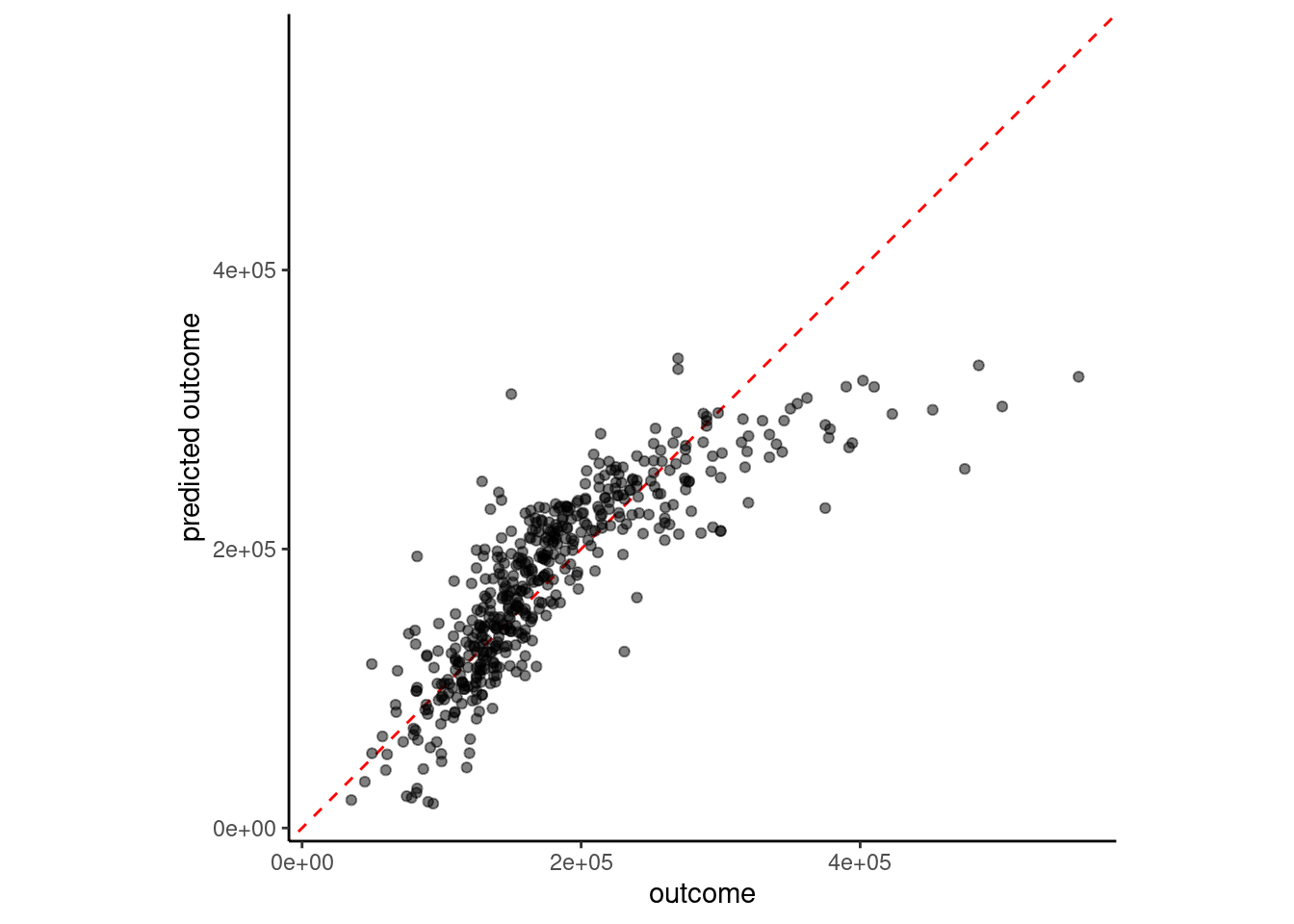

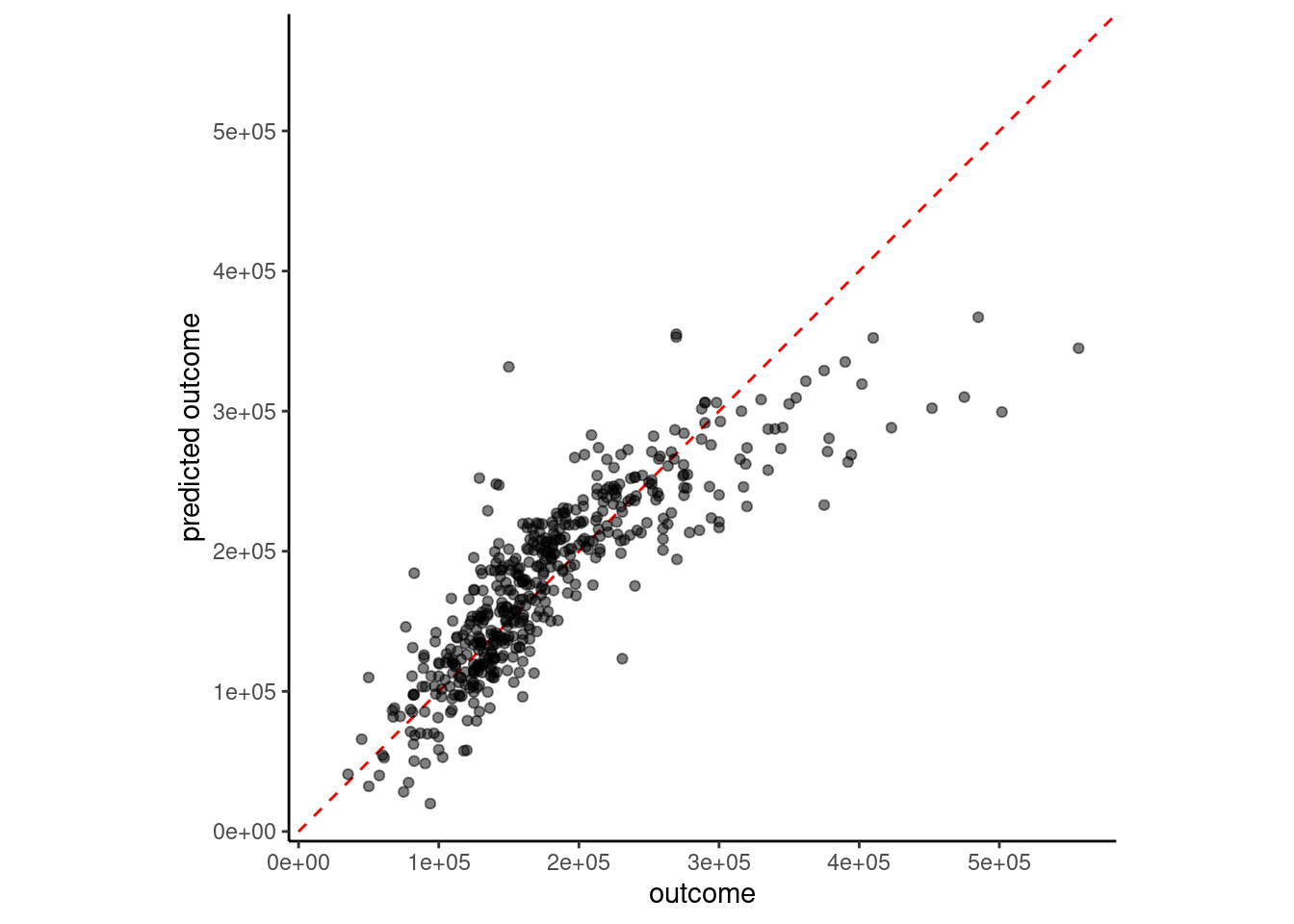

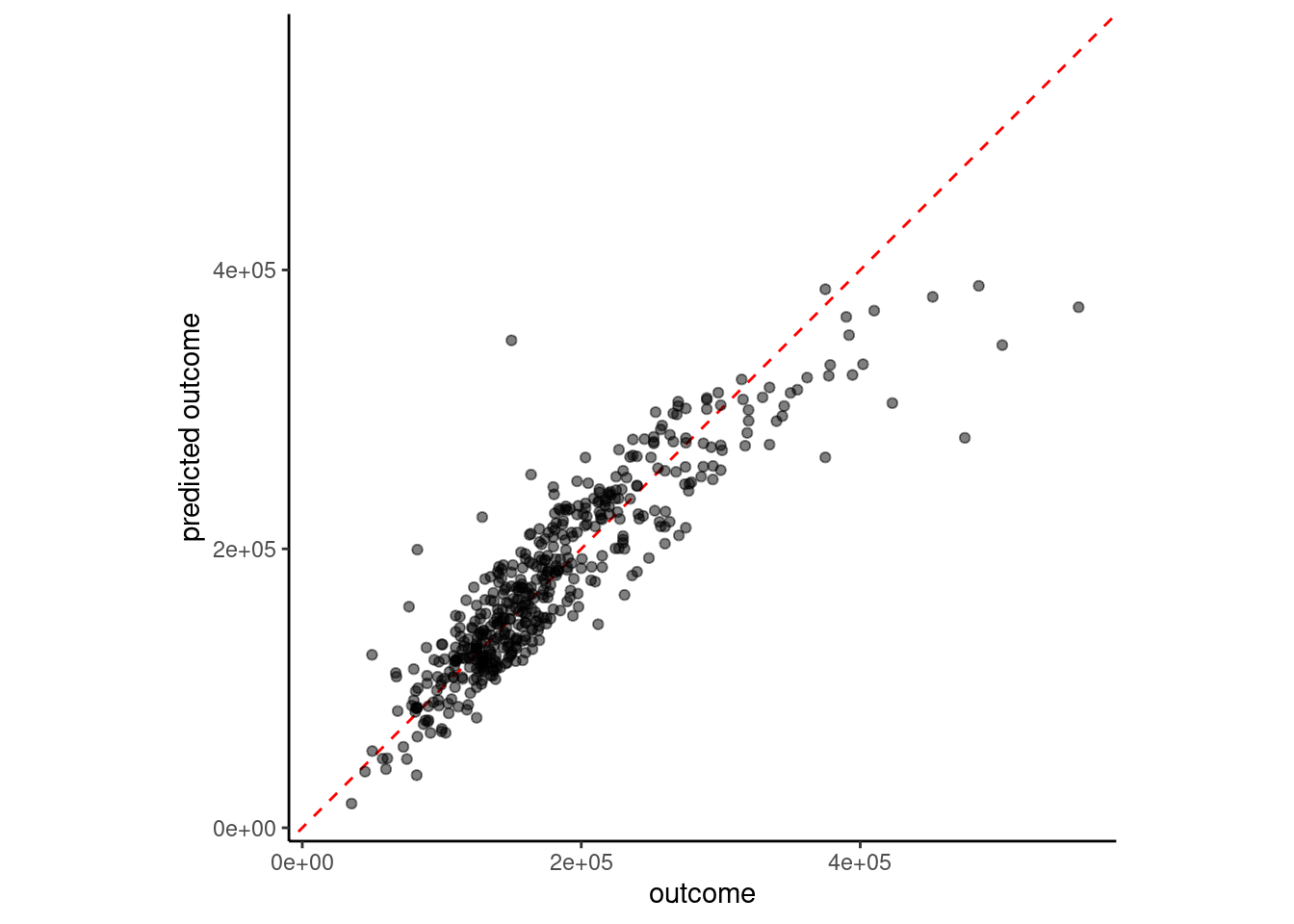

# ℹ 480 more rowsWe can visualize how well this model performs in the validation set by plotting predicted sale_price (\(\hat{sale\_price}\)) vs. sale_price (ground truth in machine learning terminology) for these data

We might do this a lot so let’s write a function. We have also included this function in fun_ml.R

plot_truth <- function(truth, estimate) {

ggplot(mapping = aes(x = truth, y = estimate)) +

geom_abline(lty = 2, color = "red") +

geom_point(alpha = 0.5) +

labs(y = "predicted outcome", x = "outcome") +

coord_obs_pred() # scale axes uniformly (from tune package)

}plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_1, feat_val)$.pred)

Perfect performance would have all the points right on the dotted line (same value for actual and predicted outcome)

sale_price and gr_liv_area were positively skewedWe can quantify model performance by selecting a performance metric

yardstick package within the tidymodels framework supports calculation of many performance metrics for regression and classification modelsRoot mean square error (RMSE) is a common performance metric for regression models

rmse_vec() from the yardstick packagermse_vec(truth = feat_val$sale_price,

estimate = predict(fit_lm_1, feat_val)$.pred)[1] 51375.08Let’s record how well this model performed in validation so we can compare it to subsequent models

error_val <- bind_rows(error_val,

tibble(model = "simple linear model",

rmse_val = rmse_vec(truth = feat_val$sale_price,

estimate = predict(fit_lm_1,

feat_val)$.pred)))

error_val# A tibble: 1 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.NOTE: I will continue to bind RMSE to this dataframe for newer models but plan to hide this code chuck to avoid distractions. You can reuse this code repeatedly to track your own models if you like. (Perhaps we should write a function??)

For explanatory purposes, we might want to visualize the relationship between a feature and the outcome (in addition to examining the parameter estimates and the associated statistical tests)

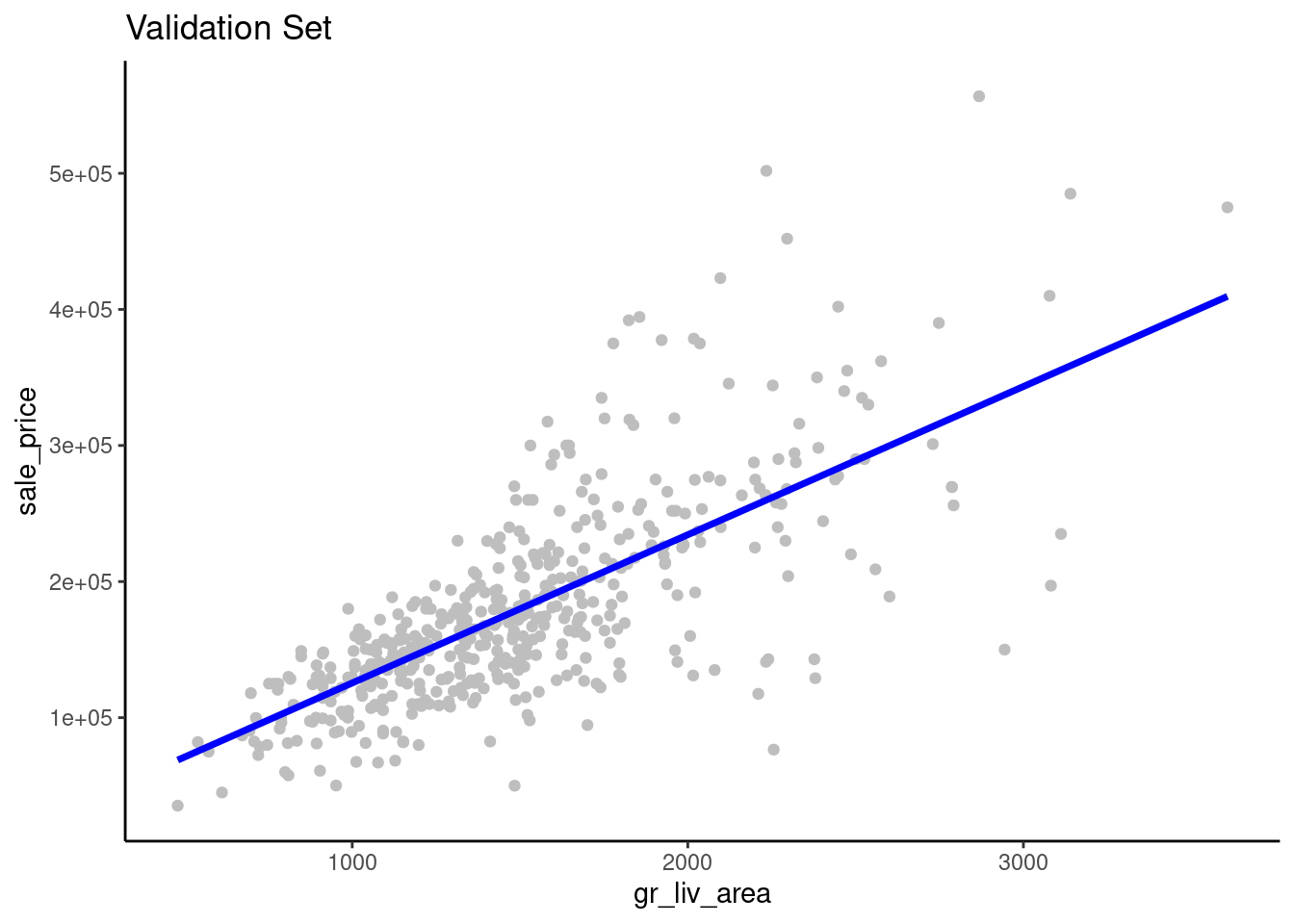

gr_liv_area superimposed over a scatterplot of the raw data from the validation setfeat_val |>

ggplot(aes(x = gr_liv_area)) +

geom_point(aes(y = sale_price), color = "gray") +

geom_line(aes(y = predict(fit_lm_1, data_val)$.pred),

linewidth = 1.25, color = "blue") +

ggtitle("Validation Set")

gr_liv_area and sale_price.sale_price (or gr_liv_area)We can improve model performance by moving from simple linear model to a linear model with multiple features derived from multiple predictors

We have many other numeric variables available to use, even in this pared down version of the dataset.

data_trn |> names() [1] "sale_price" "gr_liv_area" "lot_area" "year_built" "overall_qual"

[6] "garage_cars" "garage_qual" "ms_zoning" "lot_config" "bldg_type" Let’s expand our model to also include lot_area, year_built, and garage_cars

Again, we need:

With the addition of new predictors, we now have a feature engineering task

garage_cars in the training setA simple solution is to do median imputation - substitute the median of the non-missing scores for any missing score.

tidymodels websiteLet’s add this to our recipe. All of the defaults are appropriate but you should see ?step_impute_median() to review them

rec <-

1 recipe(sale_price ~ gr_liv_area + lot_area + year_built + garage_cars,

data = data_trn) |>

step_impute_median(garage_cars)+ between them

Now we need to

rec_prep <- rec |>

1 prep(data_trn)training = at this point. Remember, we prep recipes with training data.

feat_trn <- rec_prep |>

1 bake(data_trn)new_data = but remember, we use NULL if we want the previously saved training features. If instead, we want features for new data, we provide that dataset.

garage_qualfeat_trn |> skim_all()| Name | feat_trn |

| Number of rows | 1465 |

| Number of columns | 5 |

| _______________________ | |

| Column type frequency: | |

| numeric | 5 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1506.84 | 511.44 | 438 | 1128 | 1450 | 1759 | 5642 | 1.43 | 5.19 |

| lot_area | 0 | 1 | 10144.16 | 8177.55 | 1476 | 7500 | 9375 | 11362 | 164660 | 11.20 | 182.91 |

| year_built | 0 | 1 | 1971.35 | 29.65 | 1880 | 1953 | 1972 | 2000 | 2010 | -0.54 | -0.62 |

| garage_cars | 0 | 1 | 1.78 | 0.76 | 0 | 1 | 2 | 2 | 4 | -0.26 | 0.10 |

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789 | 129500 | 160000 | 213500 | 745000 | 1.64 | 4.60 |

feat_val <- rec_prep |>

1 bake(data_val)data_val

feat_val |> skim_all()| Name | feat_val |

| Number of rows | 490 |

| Number of columns | 5 |

| _______________________ | |

| Column type frequency: | |

| numeric | 5 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1493.00 | 483.78 | 480 | 1143.5 | 1436.0 | 1729.50 | 3608 | 0.92 | 1.16 |

| lot_area | 0 | 1 | 10462.08 | 10422.55 | 1680 | 7500.0 | 9563.5 | 11780.75 | 215245 | 15.64 | 301.66 |

| year_built | 0 | 1 | 1971.08 | 30.96 | 1875 | 1954.0 | 1975.0 | 2000.00 | 2010 | -0.66 | -0.41 |

| garage_cars | 0 | 1 | 1.74 | 0.76 | 0 | 1.0 | 2.0 | 2.00 | 4 | -0.24 | 0.22 |

| sale_price | 0 | 1 | 178512.82 | 75493.59 | 35311 | 129125.0 | 160000.0 | 213000.00 | 556581 | 1.42 | 2.97 |

Now let’s combine our algorithm and training features to fit this model configuration with 4 features

fit_lm_4 <-

linear_reg() |>

set_engine("lm") |>

1 fit(sale_price ~ ., data = feat_trn). is a bit more useful now

This yields these parameter estimates (which as we know from 610/710 were selected to minimize SSE in the training set):

fit_lm_4 |> tidy()# A tibble: 5 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -1665041. 89370. -18.6 1.14e- 69

2 gr_liv_area 76.8 2.62 29.3 3.56e-149

3 lot_area 0.514 0.146 3.51 4.60e- 4

4 year_built 854. 46.2 18.5 7.66e- 69

5 garage_cars 22901. 1964. 11.7 4.09e- 30Here is our parametric model

Compared with our previous simple regression model:

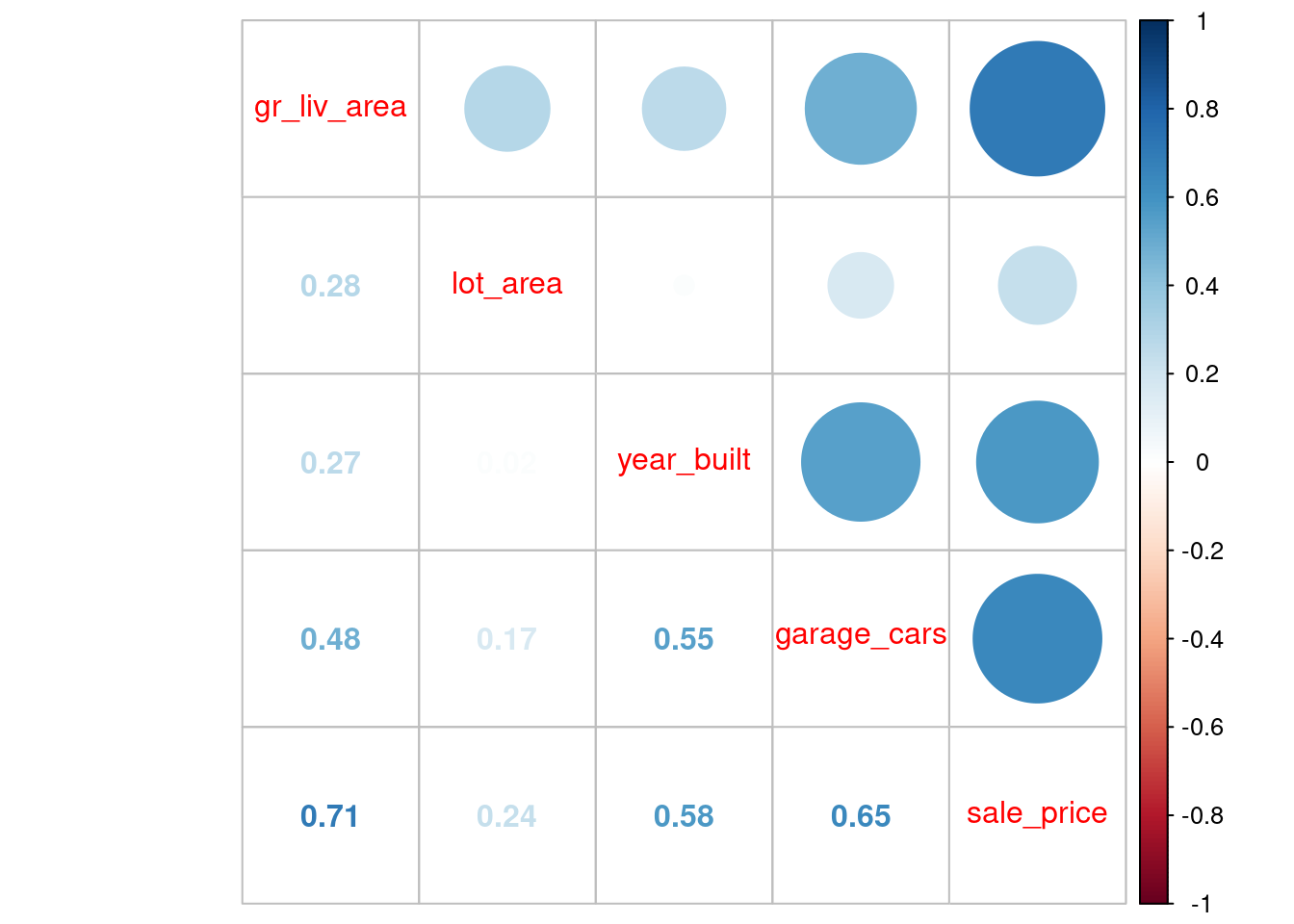

Of course, these four features are correlated both with sale_price but also with each other

Let’s look at correlations in the training set.

feat_trn |>

cor() |>

corrplot::corrplot.mixed()

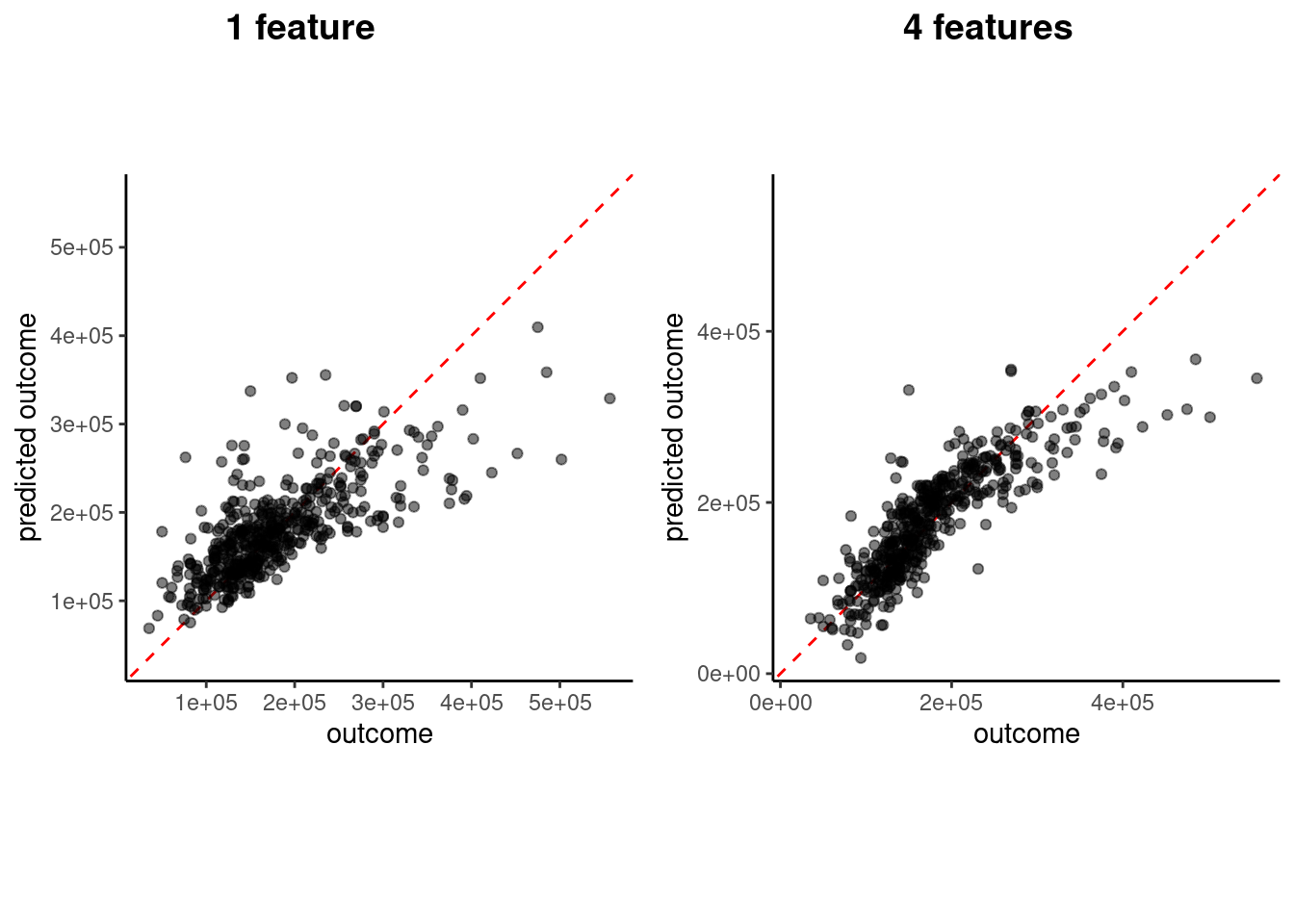

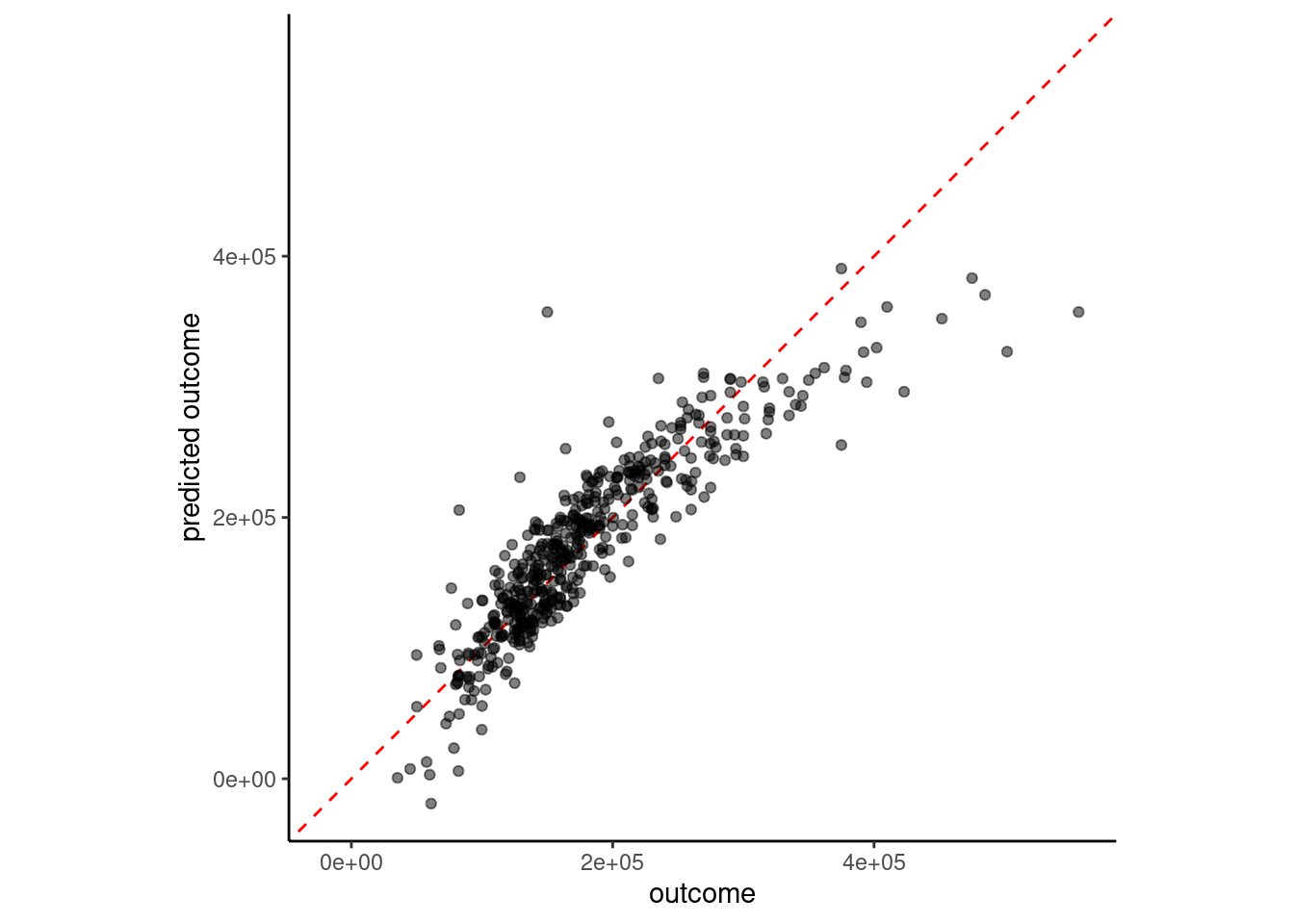

How well does this more complex model perform in validation? Let’s compare the previous and current visualizations of \(sale\_price\) vs. \(\hat{sale\_price}\)

plot_1 <- plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_1, feat_val)$.pred)

plot_4 <- plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_4, feat_val)$.pred)

cowplot::plot_grid(plot_1, plot_4,

labels = list("1 feature", "4 features"), hjust = -1.5)

Coding sidebar: Notice the use of plot_grid() from the cowplot package to make side by side plots. This also required returning the individual plots as objects (just assign to a object name, e.g., plot_1)

Let’s compare model performance for the two models using RMSE in the validation set

rmse_vec(feat_val$sale_price,

predict(fit_lm_1, feat_val)$.pred)[1] 51375.08rmse_vec(feat_val$sale_price,

predict(fit_lm_4, feat_val)$.pred)[1] 39903.25# A tibble: 2 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.Given the non-linearity suggested by the truth vs. estimate plots, we might wonder if we could improve the fit if we transformed our features to be closer to normal

There are a number of recipe functions that do transformations (see Step Functions - Individual Transformations)

We will apply step_YeoJohnson(), which is similar to a Box-Cox transformation but can be more broadly applied because the scores don’t need to be strictly positive

Let’s do it all again, now with transformed features!

rec <-

recipe(sale_price ~ gr_liv_area + lot_area + year_built + garage_cars,

data = data_trn) |>

step_impute_median(garage_cars) |>

step_YeoJohnson(lot_area, gr_liv_area, year_built, garage_cars)rec_prep <- rec |>

prep(data_trn)Use prepped recipe to bake the training set into features

Notice the features are now less skewed (but sale_price is still skewed)

feat_trn <- rec_prep |>

bake(NULL)

feat_trn |> skim_all()| Name | feat_trn |

| Number of rows | 1465 |

| Number of columns | 5 |

| _______________________ | |

| Column type frequency: | |

| numeric | 5 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 5.22 | 0.16 | 4.60 | 5.11 | 5.23 | 5.33 | 5.86 | 0.00 | 0.12 |

| lot_area | 0 | 1 | 14.10 | 1.14 | 10.32 | 13.69 | 14.20 | 14.64 | 21.65 | 0.08 | 5.46 |

| year_built | 0 | 1 | 1971.35 | 29.65 | 1880.00 | 1953.00 | 1972.00 | 2000.00 | 2010.00 | -0.54 | -0.62 |

| garage_cars | 0 | 1 | 2.12 | 0.98 | 0.00 | 1.11 | 2.37 | 2.37 | 5.23 | -0.03 | 0.04 |

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789.00 | 129500.00 | 160000.00 | 213500.00 | 745000.00 | 1.64 | 4.60 |

Use same prepped recipe to bake the validation set into features

Again, features are less skewed

feat_val <- rec_prep |>

bake(data_val)

feat_val |> skim_all()| Name | feat_val |

| Number of rows | 490 |

| Number of columns | 5 |

| _______________________ | |

| Column type frequency: | |

| numeric | 5 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 5.22 | 0.16 | 4.65 | 5.11 | 5.23 | 5.32 | 5.66 | -0.17 | 0.19 |

| lot_area | 0 | 1 | 14.14 | 1.17 | 10.57 | 13.69 | 14.24 | 14.72 | 22.44 | 0.11 | 6.12 |

| year_built | 0 | 1 | 1971.08 | 30.96 | 1875.00 | 1954.00 | 1975.00 | 2000.00 | 2010.00 | -0.66 | -0.41 |

| garage_cars | 0 | 1 | 2.06 | 0.96 | 0.00 | 1.11 | 2.37 | 2.37 | 5.23 | 0.01 | 0.24 |

| sale_price | 0 | 1 | 178512.82 | 75493.59 | 35311.00 | 129125.00 | 160000.00 | 213000.00 | 556581.00 | 1.42 | 2.97 |

fit_lm_4yj <-

linear_reg() |>

set_engine("lm") |>

fit(sale_price ~ ., data = feat_trn)plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_4yj, feat_val)$.pred)

# A tibble: 3 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.We may need to consider

sale_price (We will leave that to you for the application assignment if you are daring!)Many important predictors in our models may be categorical (nominal and some ordinal predictors)

tidymodels website for more detailsFor many algorithms, we will need to use feature engineering to convert a categorical predictor to numeric features. One common technique is to use dummy coding. When dummy coding a predictor, we transform the original categorical predictor with m levels into m-1 dummy coded features.

To better understand how and why we do this, lets consider a version of ms_zoning in the Ames dataset.

data_trn |>

pull(ms_zoning) |>

table()

agri commer float indus res_high res_low res_med

2 13 66 1 9 1157 217 We will recode ms_zoning to have only 3 levels to make our example simple (though dummy codes can be used for predictors with any number of levels)

data_dummy <- data_trn |>

1 select(sale_price, ms_zoning) |>

2 mutate(ms_zoning3 = fct_collapse(ms_zoning,

"residential" = c("res_high", "res_med",

"res_low"),

"commercial" = c("agri", "commer", "indus"),

3 "floating" = "float")) |>

4 select(-ms_zoning)sale_price and ms_zoning

fct_collapse() from the forcats package is our preferred way to collapse levels of a factor. See fct_recode() for more generic recoding of levels.

ms_zoning predictor

Take a look at the new predictor

data_dummy |>

pull(ms_zoning3) |>

table()

commercial floating residential

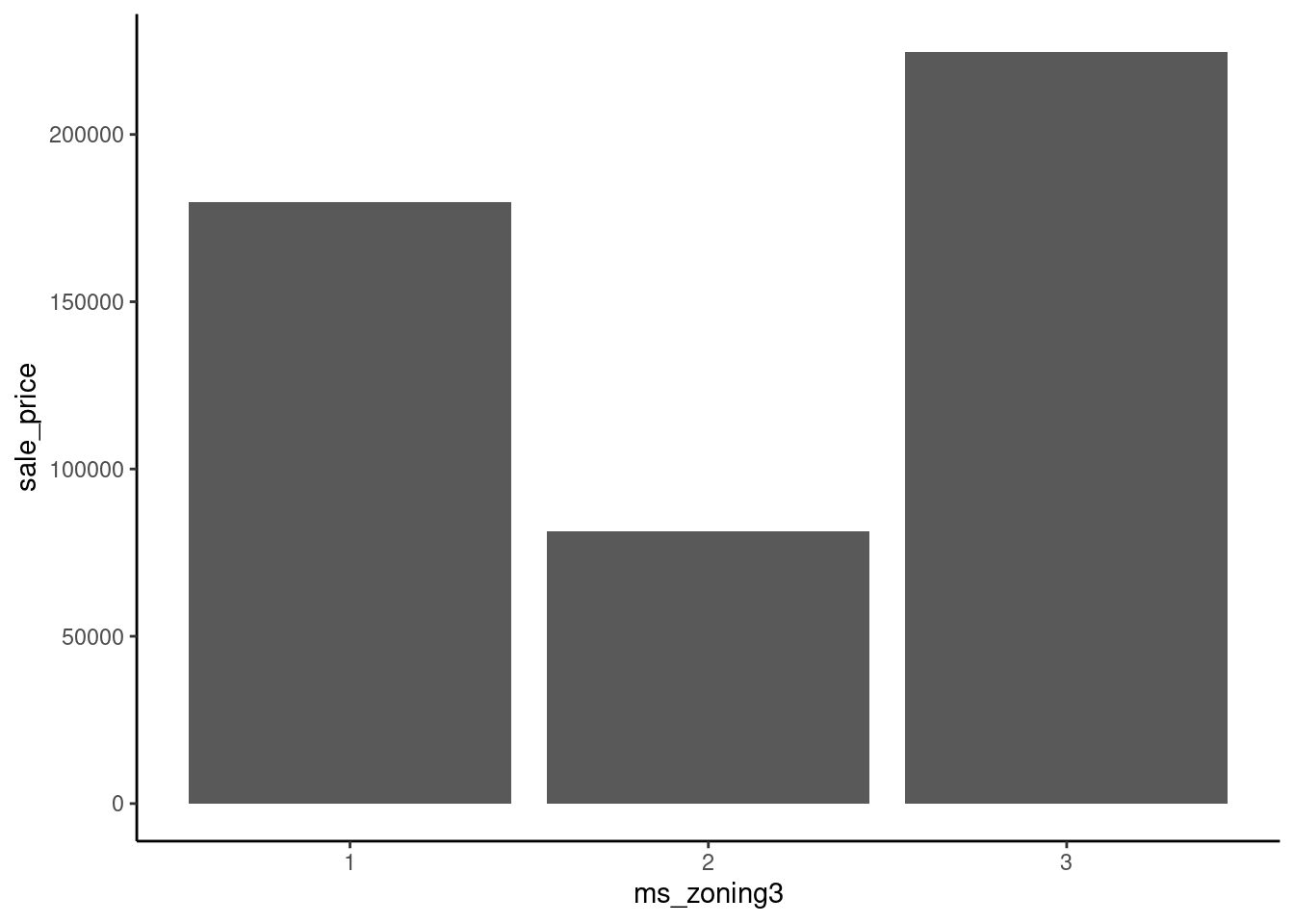

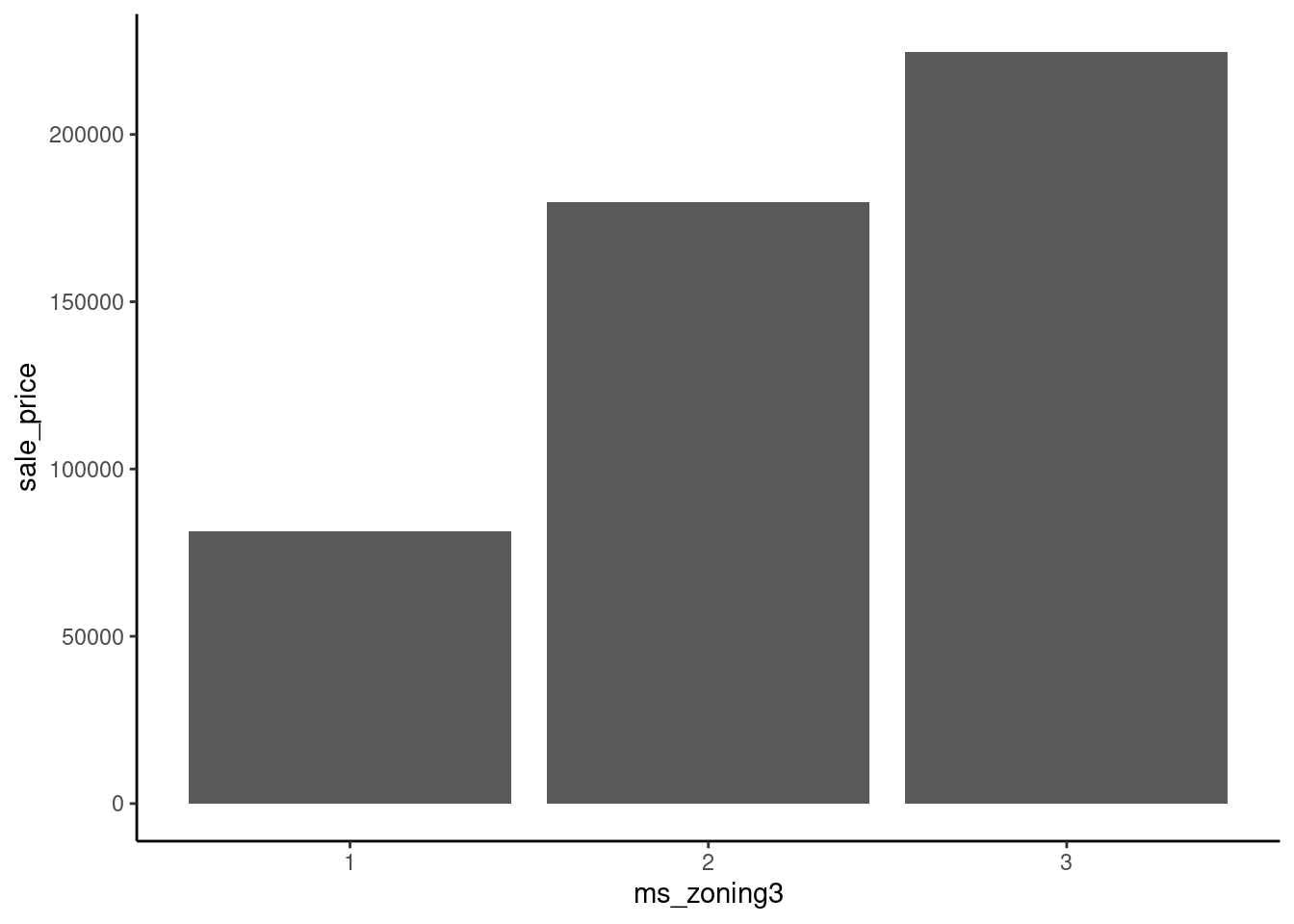

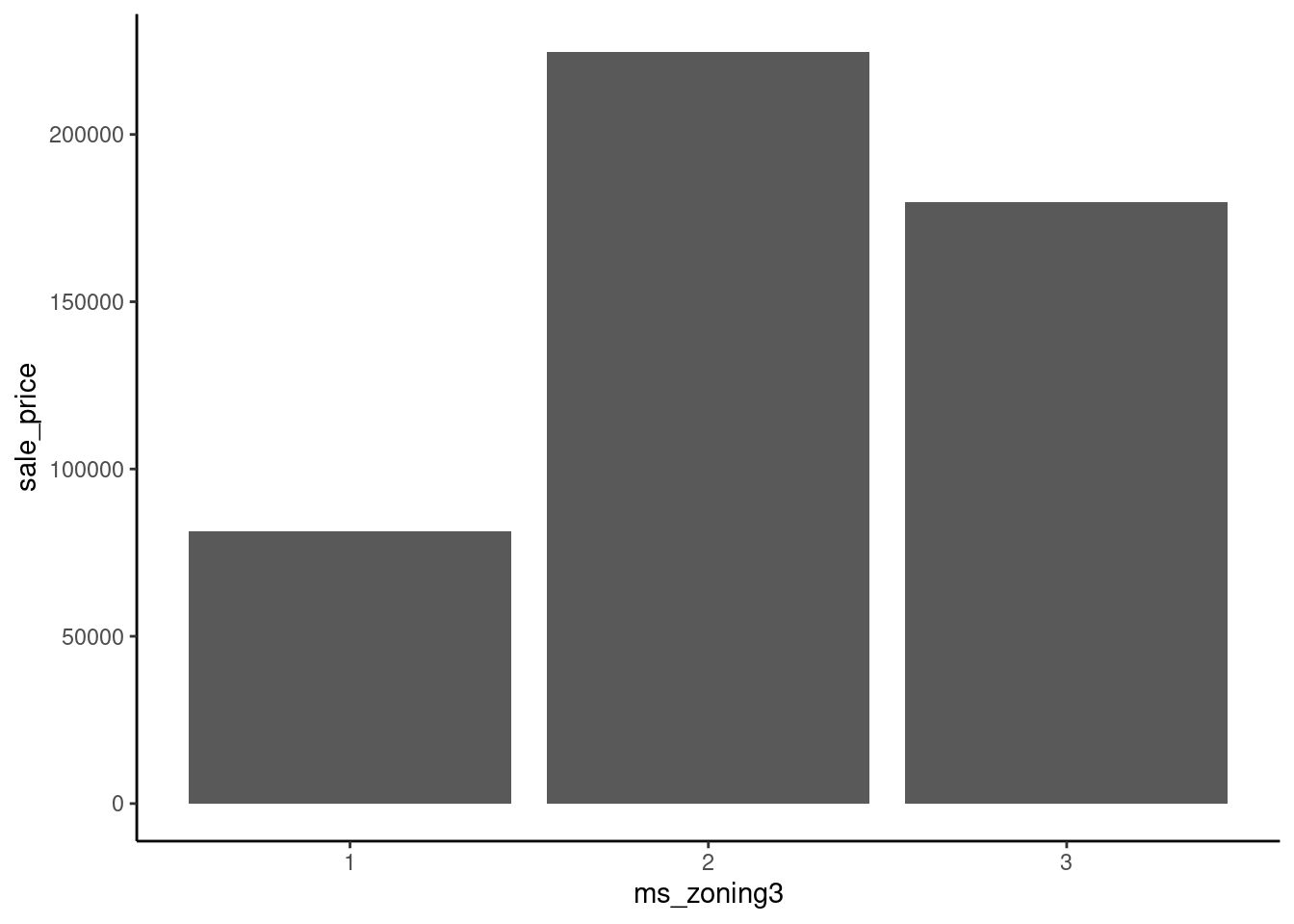

16 66 1383 Imagine fitting a straight line to predict sale_price from ms_zoning3 using these three different ways to arbitrarily assign numbers to levels.

data_dummy |>

mutate(ms_zoning3 = case_when(ms_zoning3 == "residential" ~ 1,

ms_zoning3 == "commercial" ~ 2,

ms_zoning3 == "floating" ~ 3)) |>

ggplot(aes(x = ms_zoning3, y = sale_price)) +

geom_bar(stat="summary", fun = "mean")

data_dummy |>

mutate(ms_zoning3 = case_when(ms_zoning3 == "residential" ~ 2,

ms_zoning3 == "commercial" ~ 1,

ms_zoning3 == "floating" ~ 3)) |>

ggplot(aes(x = ms_zoning3, y = sale_price)) +

geom_bar(stat="summary", fun = "mean")

data_dummy |>

mutate(ms_zoning3 = case_when(ms_zoning3 == "residential" ~ 3,

ms_zoning3 == "commercial" ~ 1,

ms_zoning3 == "floating" ~ 2)) |>

ggplot(aes(x = ms_zoning3, y = sale_price)) +

geom_bar(stat="summary", fun = "mean")

Dummy coding resolves this issue.

For example, with our three-level predictor: ms_zoning3

Here is this coding scheme displayed in a table

# A tibble: 3 × 3

ms_zoning3 d1 d2

<chr> <dbl> <dbl>

1 commercial 0 0

2 residential 1 0

3 floating 0 1With this coding:

We can add these two features manually to the data frame and view a handful of observations to make this coding scheme more concrete

# A tibble: 8 × 4

sale_price ms_zoning3 d1 d2

<dbl> <fct> <dbl> <dbl>

1 105000 residential 1 0

2 126000 residential 1 0

3 13100 commercial 0 0

4 115000 residential 1 0

5 149500 floating 0 1

6 40000 commercial 0 0

7 120000 residential 1 0

8 151000 floating 0 1If we now fit a model where we predict sale_price from these two dummy coded features, each feature would represent the contrast of the mean sale_price for the level coded 1 vs. the mean sale_price for the level that is coded 0 for all features (i.e., commercial)

sale_price for residential vs. commercialsale_price for floating vs. commercialms_zoning3 on sale_priceLets do this quickly in base R using lm() as you have done previously in 610.

m <- lm(sale_price ~ d1 + d2, data = data_dummy)

m |> summary()

Call:

lm(formula = sale_price ~ d1 + d2, data = data_dummy)

Residuals:

Min 1Q Median 3Q Max

-166952 -50241 -20241 31254 565259

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 81523 19409 4.200 2.83e-05 ***

d1 98219 19521 5.031 5.47e-07 ***

d2 143223 21634 6.620 5.03e-11 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 77640 on 1462 degrees of freedom

Multiple R-squared: 0.03151, Adjusted R-squared: 0.03018

F-statistic: 23.78 on 2 and 1462 DF, p-value: 6.858e-11The mean sale price of residential properties is 9.8219^{4} dollars higher than commercial properties.

The mean sale price of floating villages is 1.43223^{5} dollars higher than commercial properties.

To understand this conceptually, it is easiest to visualize the linear model that would predict sale_price with these two dichotomous features.

sale_price because the only possible values for d1 and d2 (which are both dichotomous) are

Statistical sidebar:

Coding Sidebar

When creating dummy coded features from factors that have levels with infrequent observations, you may occasionally end up with novel levels in your validation or test sets that were not present in your training set.

Now that we understand how to use dummy coding to feature engineer nominal predictors, let’s consider some potentially important ones that are available to us.

We can discuss if any look promising.

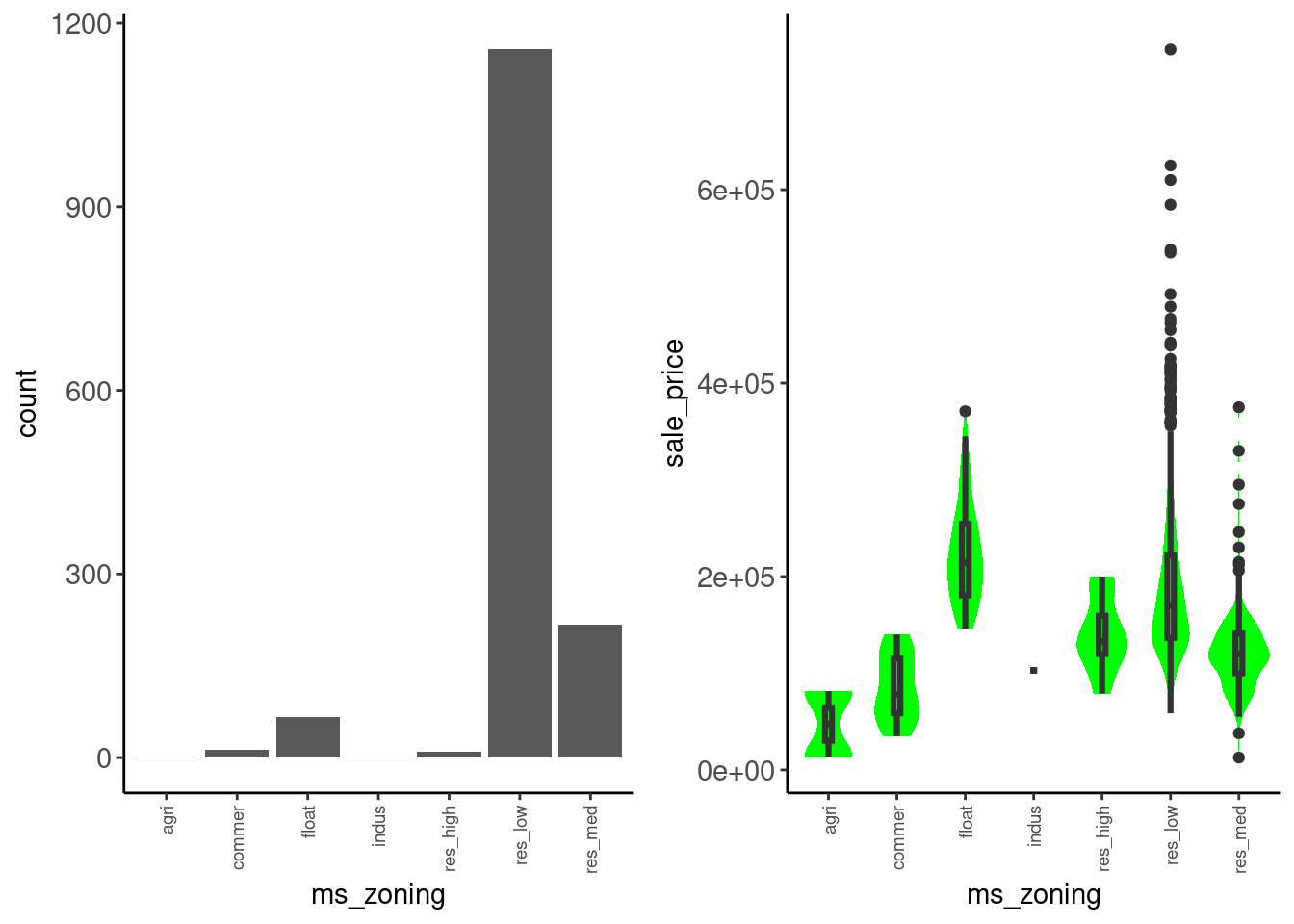

Lets return first to ms_zoning

data_trn |>

plot_categorical("ms_zoning", "sale_price") |>

cowplot::plot_grid(plotlist = _, ncol = 2)Warning: Groups with fewer than two datapoints have been dropped.

ℹ Set `drop = FALSE` to consider such groups for position adjustment purposes.

We might:

Data dictionary entry: Identifies the general zoning classification of the sale.

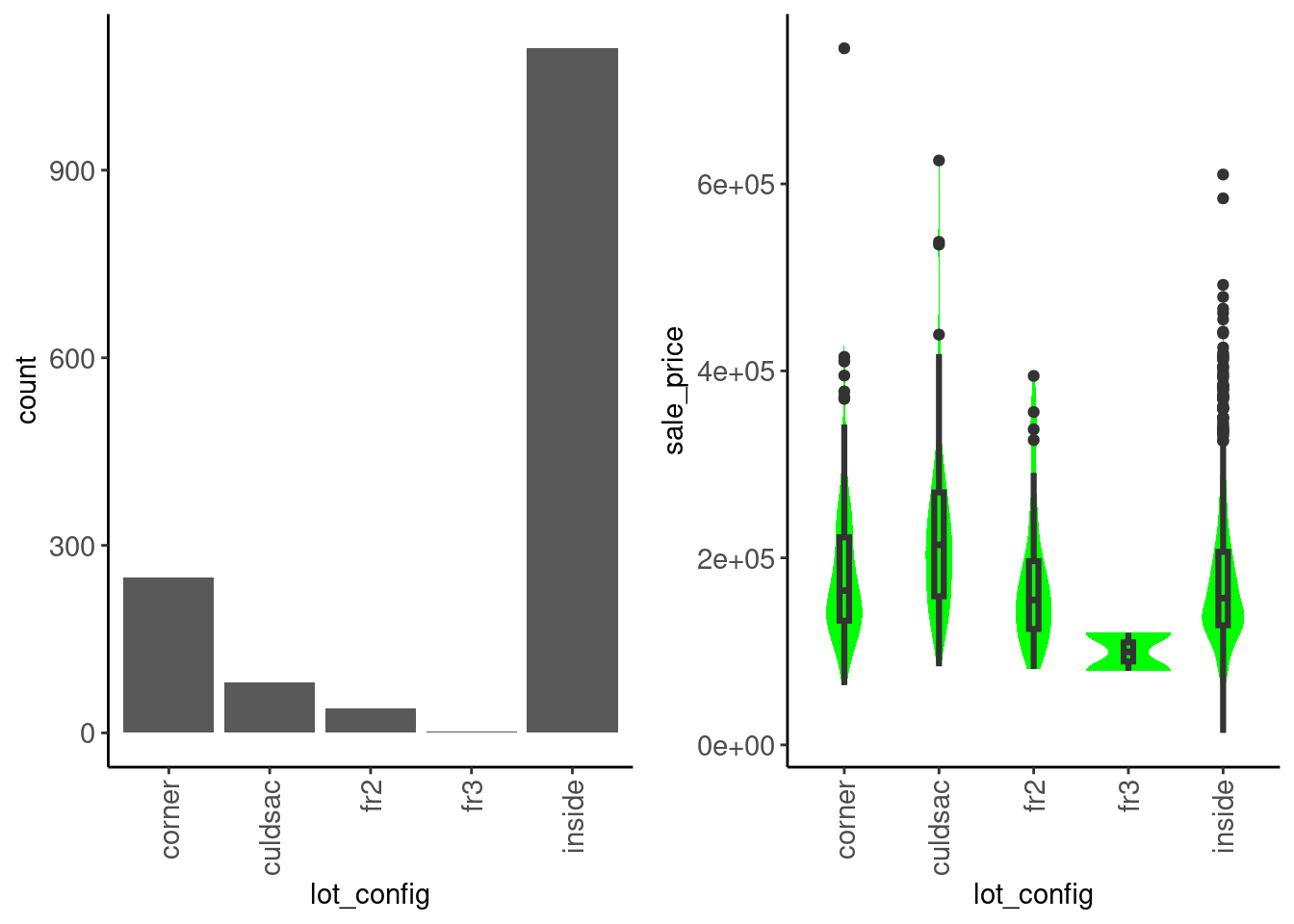

lot_config

data_trn |>

plot_categorical("lot_config", "sale_price") |>

cowplot::plot_grid(plotlist = _, ncol = 2)

We see that:

sale_price is not very different between configurationsData dictionary entry: Lot configuration

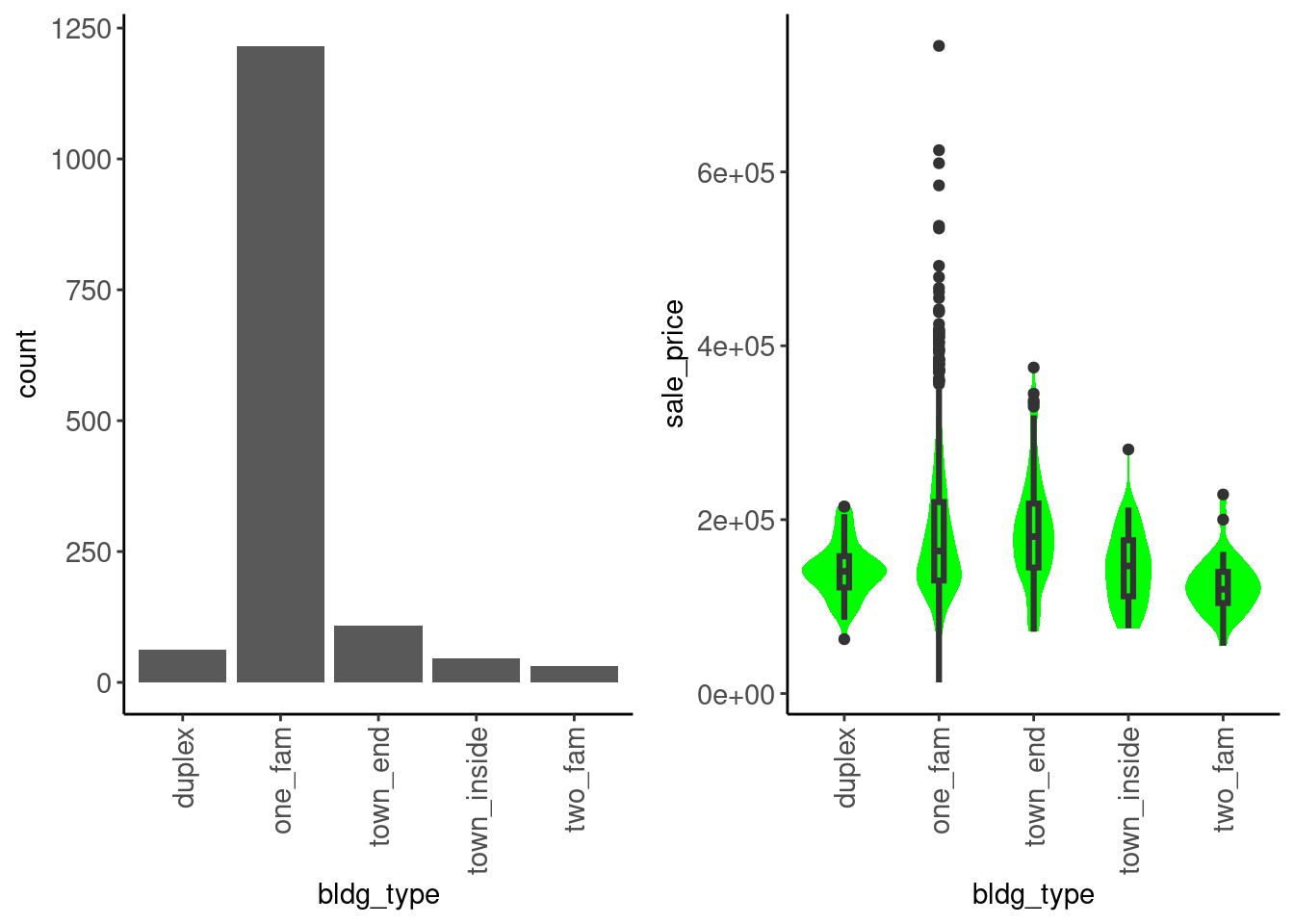

bldg_type

data_trn |>

plot_categorical("bldg_type", "sale_price") |>

cowplot::plot_grid(plotlist = _, ncol = 2)

We see that:

sale_price among categoriesData dictionary entry: Type of dwelling

Let’s do some feature engineering with ms_zoning. We can now do this formally in a recipe so that it can be used in our modeling workflow.

ms_zoning that are pretty infrequent. Lets make sure both data_trn and data_val have all levels set for this factor.data_trn |> pull(ms_zoning) |> levels()[1] "agri" "commer" "float" "indus" "res_high" "res_low" "res_med" data_val |> pull(ms_zoning) |> levels()[1] "commer" "float" "indus" "res_high" "res_low" "res_med" agri) in data_val. Lets fix that heredata_val <- data_val |>

mutate(ms_zoning = factor(ms_zoning,

levels = c("agri", "commer", "float", "indus",

"res_high", "res_low", "res_med")))[Note: Ideally, you would go back to cleaning EDA and add this level to the full dataset and then re-split into training, validation and test. This is a sloppy shortcut!]

With that fixed, let’s proceed:

step_mutate() combined with fct_collapse() to do this inside of our recipe.step_dummy(). The first level of the factor will be set to the reference level when we call step_dummy().step_dummy() is a poor choice for function name. It actually uses whatever contrast coding we have set up in R. However, the default is are dummy coded contrasts (R calls this treatment contrasts). See ?contrasts and options("contrasts") for more info.rec <-

recipe(sale_price ~ gr_liv_area + lot_area + year_built + garage_cars + ms_zoning,

data = data_trn) |>

step_impute_median(garage_cars) |>

step_mutate(ms_zoning = fct_collapse(ms_zoning,

"residential" = c("res_high", "res_med", "res_low"),

"commercial" = c("agri", "commer", "indus"),

"floating" = "float")) |>

step_dummy(ms_zoning)Coding Sidebar

You should also read more about some other step_() functions that you might use for categorical predictors: - step_other() to combine all low frequency categories into a single “other” category. - step_unknown() to assign missing values their own category - You can use selector functions. For example, you could make dummy variables out of all of your factors in one step using step_dummy(all_nominal_predictors()).

See the Step Functions - Dummy Variables and Encoding section on the tidymodels website for additional useful functions.

We have also described these in the section on factor steps in Appendix 1

Let’s see if the addition of ms_zoning helped

ms_zoningrec_prep <- rec |>

prep(data_trn)

feat_trn <- rec_prep |>

bake(NULL)

feat_val <- rec_prep |>

bake(data_val)feat_trn |> skim_all()| Name | feat_trn |

| Number of rows | 1465 |

| Number of columns | 7 |

| _______________________ | |

| Column type frequency: | |

| numeric | 7 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1506.84 | 511.44 | 438 | 1128 | 1450 | 1759 | 5642 | 1.43 | 5.19 |

| lot_area | 0 | 1 | 10144.16 | 8177.55 | 1476 | 7500 | 9375 | 11362 | 164660 | 11.20 | 182.91 |

| year_built | 0 | 1 | 1971.35 | 29.65 | 1880 | 1953 | 1972 | 2000 | 2010 | -0.54 | -0.62 |

| garage_cars | 0 | 1 | 1.78 | 0.76 | 0 | 1 | 2 | 2 | 4 | -0.26 | 0.10 |

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789 | 129500 | 160000 | 213500 | 745000 | 1.64 | 4.60 |

| ms_zoning_floating | 0 | 1 | 0.05 | 0.21 | 0 | 0 | 0 | 0 | 1 | 4.38 | 17.22 |

| ms_zoning_residential | 0 | 1 | 0.94 | 0.23 | 0 | 1 | 1 | 1 | 1 | -3.86 | 12.90 |

feat_val |> skim_all()| Name | feat_val |

| Number of rows | 490 |

| Number of columns | 7 |

| _______________________ | |

| Column type frequency: | |

| numeric | 7 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1493.00 | 483.78 | 480 | 1143.5 | 1436.0 | 1729.50 | 3608 | 0.92 | 1.16 |

| lot_area | 0 | 1 | 10462.08 | 10422.55 | 1680 | 7500.0 | 9563.5 | 11780.75 | 215245 | 15.64 | 301.66 |

| year_built | 0 | 1 | 1971.08 | 30.96 | 1875 | 1954.0 | 1975.0 | 2000.00 | 2010 | -0.66 | -0.41 |

| garage_cars | 0 | 1 | 1.74 | 0.76 | 0 | 1.0 | 2.0 | 2.00 | 4 | -0.24 | 0.22 |

| sale_price | 0 | 1 | 178512.82 | 75493.59 | 35311 | 129125.0 | 160000.0 | 213000.00 | 556581 | 1.42 | 2.97 |

| ms_zoning_floating | 0 | 1 | 0.05 | 0.22 | 0 | 0.0 | 0.0 | 0.00 | 1 | 4.07 | 14.58 |

| ms_zoning_residential | 0 | 1 | 0.93 | 0.25 | 0 | 1.0 | 1.0 | 1.00 | 1 | -3.51 | 10.33 |

fit_lm_6 <-

linear_reg() |>

set_engine("lm") |>

fit(sale_price ~ ., data = feat_trn)plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_6, feat_val)$.pred)

# A tibble: 4 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.ms_zoning may have helped a littleWe have two paths to pursue for ordinal predictors

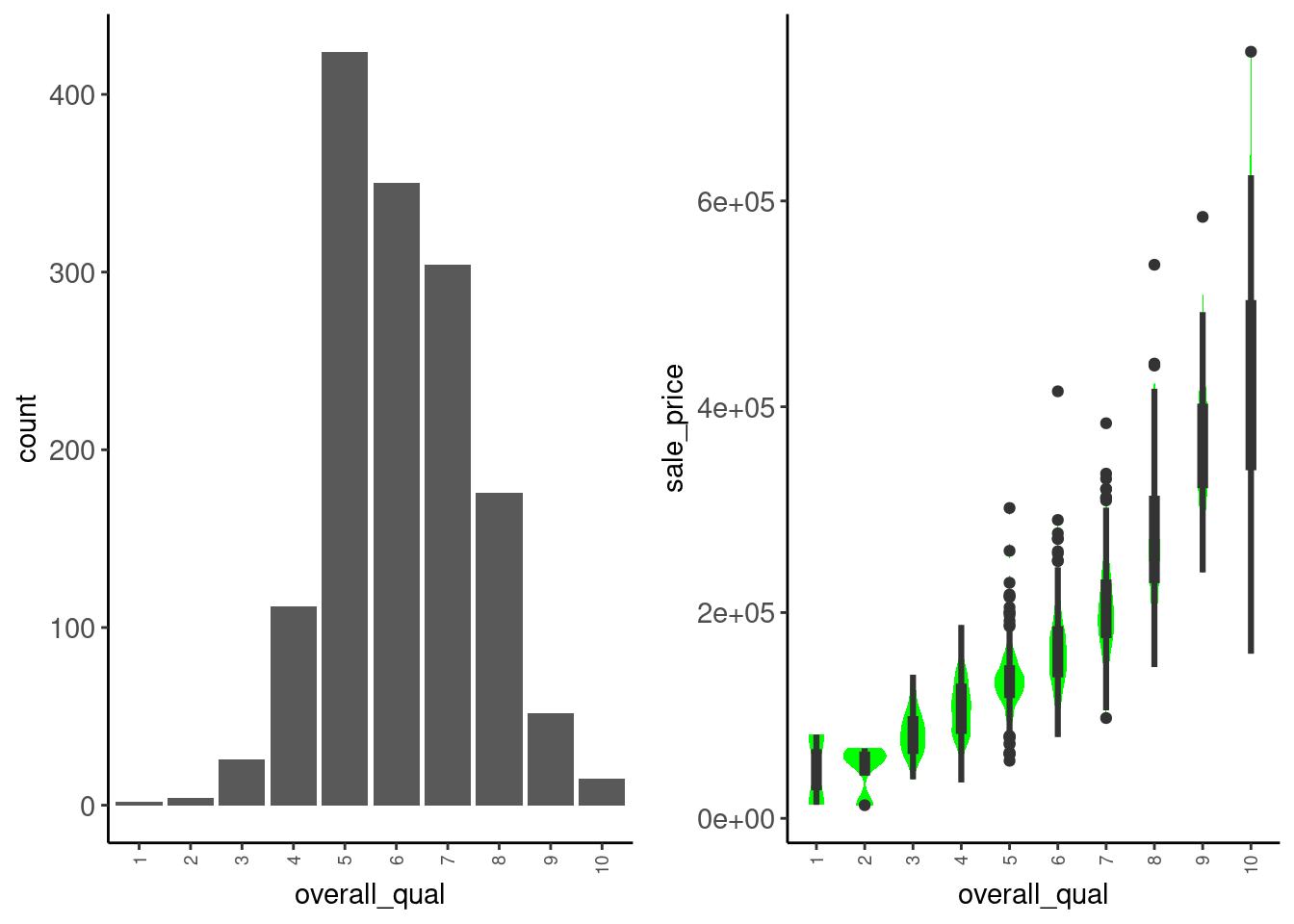

Let’s consider overall_qual

data_trn |>

plot_categorical("overall_qual", "sale_price") |>

cowplot::plot_grid(plotlist = _, ncol = 2)

Observations:

sale_price. Treat as numeric?Let’s add overall_qual to our model as numeric

Remember that this predictor was ordinal so we paid special attention to the order of the levels when we classed this factor. Lets confirm they are in order

data_trn |> pull(overall_qual) |> levels() [1] "1" "2" "3" "4" "5" "6" "7" "8" "9" "10"To convert overall_qual to numeric (with levels in the specified order), we can use another simple mutate inside our recipe.

rec <-

recipe(sale_price ~ ~ gr_liv_area + lot_area + year_built + garage_cars +

ms_zoning + overall_qual, data = data_trn) |>

step_impute_median(garage_cars) |>

step_mutate(ms_zoning = fct_collapse(ms_zoning,

"residential" = c("res_high", "res_med", "res_low"),

"commercial" = c("agri", "commer", "indus"),

"floating" = "float"),

overall_qual = as.numeric(overall_qual)) |>

step_dummy(ms_zoning)Coding Sidebar

There is a step function called step_ordinalscore() but it requires that the factor is classed as an ordered factor. It is also more complicated than needed in our opinion. Just use as.numeric()

Let’s evaluate this model

rec_prep <- rec |>

prep(data_trn)

feat_trn <- rec_prep |>

bake(NULL)

feat_val <- rec_prep |>

bake(data_val)fit_lm_7 <-

linear_reg() |>

set_engine("lm") |>

fit(sale_price ~ ., data = feat_trn)plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_7, feat_val)$.pred)

# A tibble: 5 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.

5 7 feature linear model 34080.There may be interactive effects among our predictors

For example, it may be that the relationship between year_built and sale_price depends on overall_qual.

In the tidymodels framework

tidymodels websiterec <-

recipe(sale_price ~ ~ gr_liv_area + lot_area + year_built + garage_cars +

ms_zoning + overall_qual, data = data_trn) |>

step_impute_median(garage_cars) |>

step_mutate(ms_zoning = fct_collapse(ms_zoning,

"residential" = c("res_high", "res_med", "res_low"),

"commercial" = c("agri", "commer", "indus"),

"floating" = "float"),

overall_qual = as.numeric(overall_qual)) |>

step_dummy(ms_zoning) |>

step_interact(~ overall_qual:year_built)Let’s prep, bake, fit, and evaluate!

rec_prep <- rec |>

prep(data_trn)

feat_trn <- rec_prep |>

bake(NULL)

feat_val <- rec_prep |>

bake(data_val)feat_trn here)feat_trn |> skim_all()| Name | feat_trn |

| Number of rows | 1465 |

| Number of columns | 9 |

| _______________________ | |

| Column type frequency: | |

| numeric | 9 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1506.84 | 511.44 | 438 | 1128 | 1450 | 1759 | 5642 | 1.43 | 5.19 |

| lot_area | 0 | 1 | 10144.16 | 8177.55 | 1476 | 7500 | 9375 | 11362 | 164660 | 11.20 | 182.91 |

| year_built | 0 | 1 | 1971.35 | 29.65 | 1880 | 1953 | 1972 | 2000 | 2010 | -0.54 | -0.62 |

| garage_cars | 0 | 1 | 1.78 | 0.76 | 0 | 1 | 2 | 2 | 4 | -0.26 | 0.10 |

| overall_qual | 0 | 1 | 6.08 | 1.41 | 1 | 5 | 6 | 7 | 10 | 0.20 | -0.03 |

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789 | 129500 | 160000 | 213500 | 745000 | 1.64 | 4.60 |

| ms_zoning_floating | 0 | 1 | 0.05 | 0.21 | 0 | 0 | 0 | 0 | 1 | 4.38 | 17.22 |

| ms_zoning_residential | 0 | 1 | 0.94 | 0.23 | 0 | 1 | 1 | 1 | 1 | -3.86 | 12.90 |

| overall_qual_x_year_built | 0 | 1 | 12015.69 | 2907.93 | 1951 | 9800 | 11808 | 14021 | 20090 | 0.24 | -0.11 |

fit_lm_8 <-

linear_reg() |>

set_engine("lm") |>

fit(sale_price ~.,

data = feat_trn)plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_8, feat_val)$.pred)

# A tibble: 6 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.

5 7 feature linear model 34080.

6 8 feature linear model w/interaction 32720.You can also feature engineer interactions with nominal (and ordinal predictors treated as nominal) predictors

starts_with() or matches() to make it easy if there are many features associated with a categorical predictorLet’s code an interaction between ms_zoning & year_built.

ms_zoning wasn’t usefulrec <-

recipe(sale_price ~ ~ gr_liv_area + lot_area + year_built + garage_cars +

ms_zoning + overall_qual, data = data_trn) |>

step_impute_median(garage_cars) |>

step_mutate(ms_zoning = fct_collapse(ms_zoning,

"residential" = c("res_high", "res_med", "res_low"),

"commercial" = c("agri", "commer", "indus"),

"floating" = "float"),

overall_qual = as.numeric(overall_qual)) |>

step_dummy(ms_zoning) |>

step_interact(~ overall_qual:year_built) |>

step_interact(~ starts_with("ms_zoning_"):year_built) rec_prep <- rec |>

prep(data_trn)

feat_trn <- rec_prep |>

bake(NULL)

feat_val <- rec_prep |>

bake(data_val)feat_trn |> skim_all()| Name | feat_trn |

| Number of rows | 1465 |

| Number of columns | 11 |

| _______________________ | |

| Column type frequency: | |

| numeric | 11 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 1506.84 | 511.44 | 438 | 1128 | 1450 | 1759 | 5642 | 1.43 | 5.19 |

| lot_area | 0 | 1 | 10144.16 | 8177.55 | 1476 | 7500 | 9375 | 11362 | 164660 | 11.20 | 182.91 |

| year_built | 0 | 1 | 1971.35 | 29.65 | 1880 | 1953 | 1972 | 2000 | 2010 | -0.54 | -0.62 |

| garage_cars | 0 | 1 | 1.78 | 0.76 | 0 | 1 | 2 | 2 | 4 | -0.26 | 0.10 |

| overall_qual | 0 | 1 | 6.08 | 1.41 | 1 | 5 | 6 | 7 | 10 | 0.20 | -0.03 |

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789 | 129500 | 160000 | 213500 | 745000 | 1.64 | 4.60 |

| ms_zoning_floating | 0 | 1 | 0.05 | 0.21 | 0 | 0 | 0 | 0 | 1 | 4.38 | 17.22 |

| ms_zoning_residential | 0 | 1 | 0.94 | 0.23 | 0 | 1 | 1 | 1 | 1 | -3.86 | 12.90 |

| overall_qual_x_year_built | 0 | 1 | 12015.69 | 2907.93 | 1951 | 9800 | 11808 | 14021 | 20090 | 0.24 | -0.11 |

| ms_zoning_floating_x_year_built | 0 | 1 | 90.29 | 415.84 | 0 | 0 | 0 | 0 | 2009 | 4.38 | 17.22 |

| ms_zoning_residential_x_year_built | 0 | 1 | 1860.03 | 453.95 | 0 | 1948 | 1968 | 1997 | 2010 | -3.83 | 12.78 |

fit_lm_10 <-

linear_reg() |>

set_engine("lm") |>

fit(sale_price ~ ., data = feat_trn)plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_lm_10, feat_val)$.pred)

error_val <- error_val |>

bind_rows(tibble(model = "10 feature linear model w/interactions",

rmse_val = rmse_vec(feat_val$sale_price,

predict(fit_lm_10,

feat_val)$.pred)))

error_val# A tibble: 7 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.

5 7 feature linear model 34080.

6 8 feature linear model w/interaction 32720.

7 10 feature linear model w/interactions 32708.We may also want to model non-linear effects of our predictors

tidymodels websitestep_poly())K Nearest Neighbor

K Nearest Neighbor

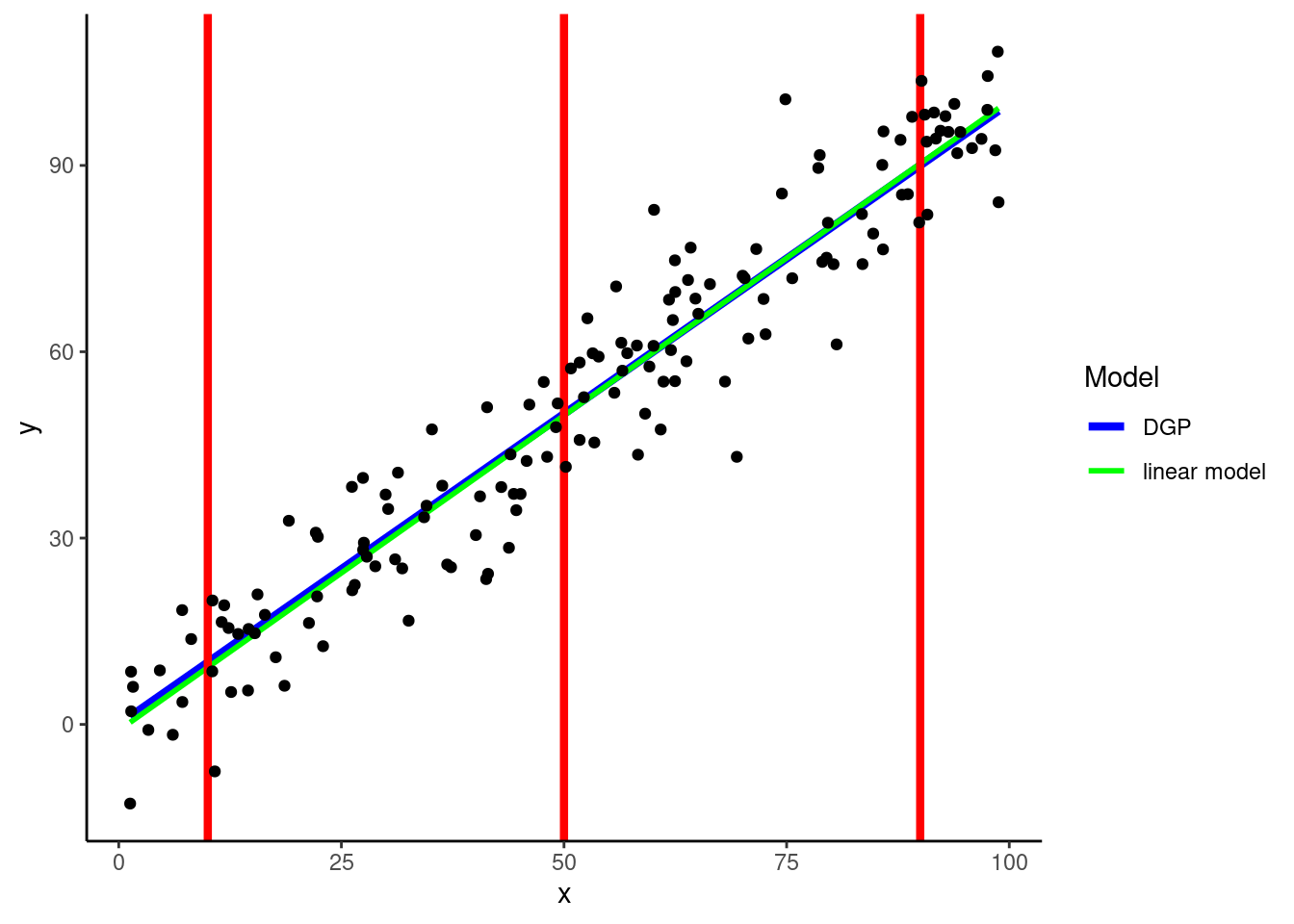

To better understand KNN let’s simulate training data for three different DGPs (linear - y, polynomial - y2, and step - y3)

Let’s start with a simple example where the DGP for Y is linear on one predictor (X)

DGP: \(y = rnorm(150, x, 10)\)

This figure displays:

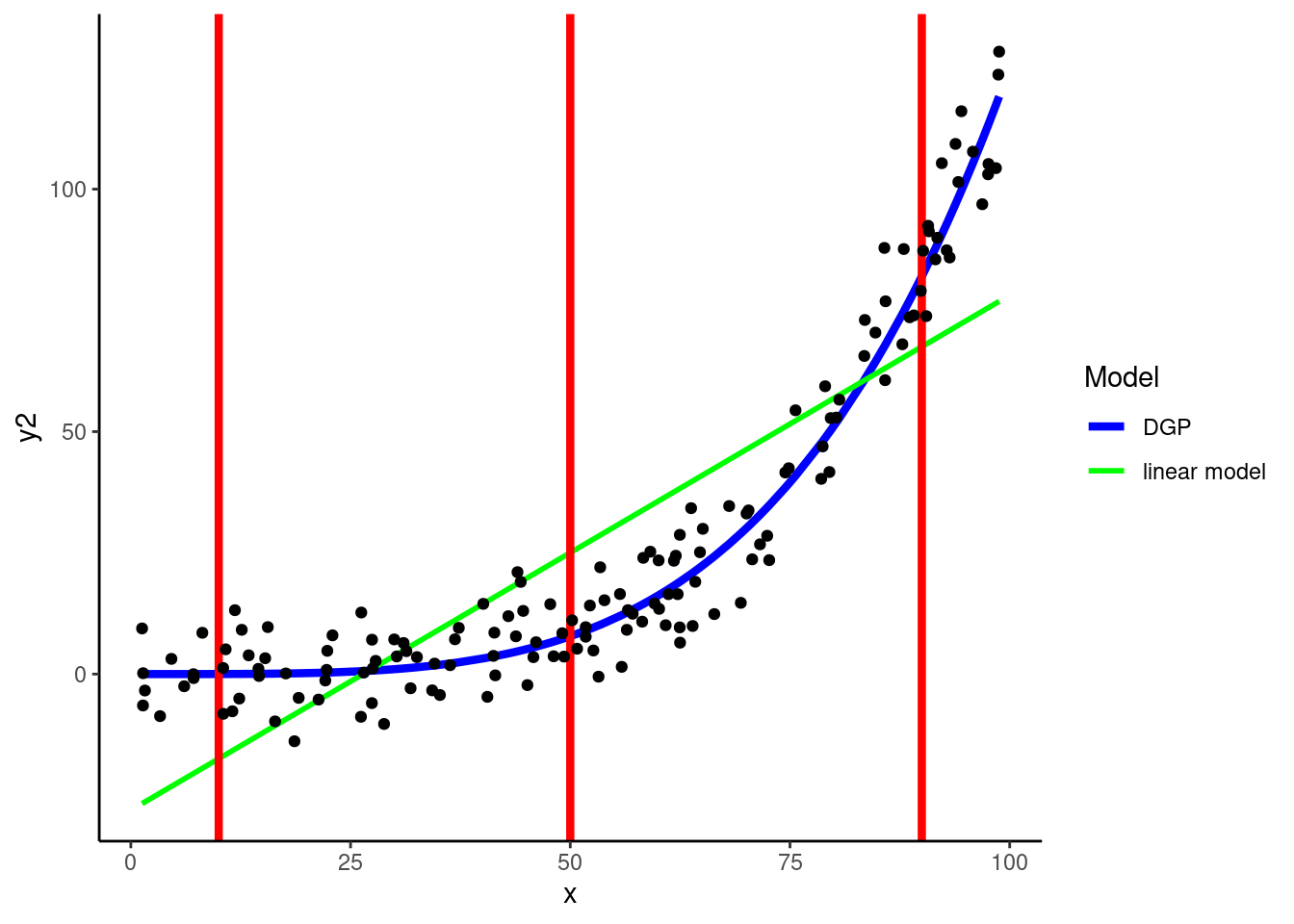

KNN can easily accommodate non-linear relationships between numeric predictors and outcomes without any feature engineering for predictors

In fact, it can flexibly handle any shape of relationship

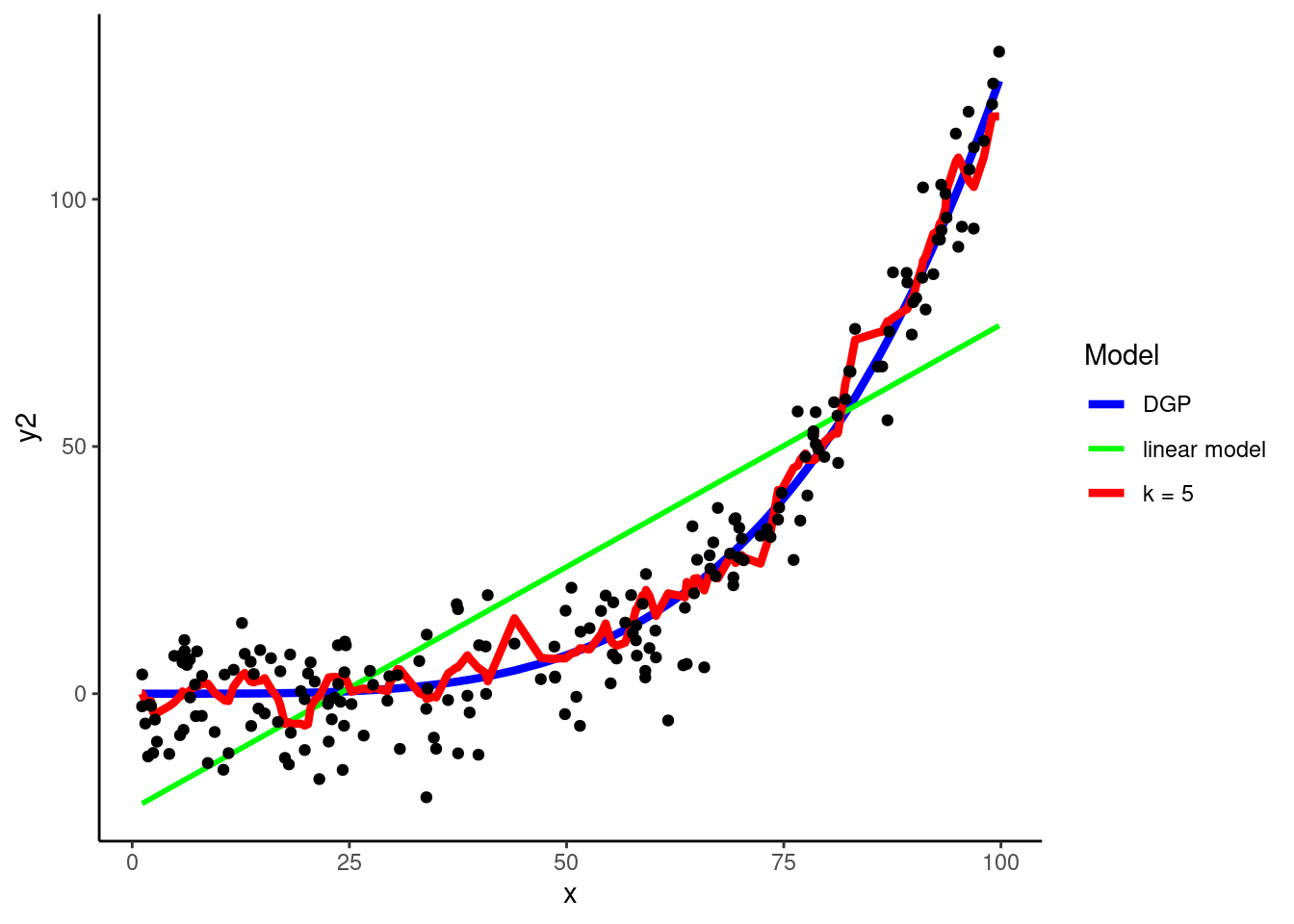

DGP: \(y2 = rnorm(150, x^4 / 800000, 8)\)

Warning: Using `size` aesthetic for lines was deprecated in ggplot2 3.4.0.

ℹ Please use `linewidth` instead.

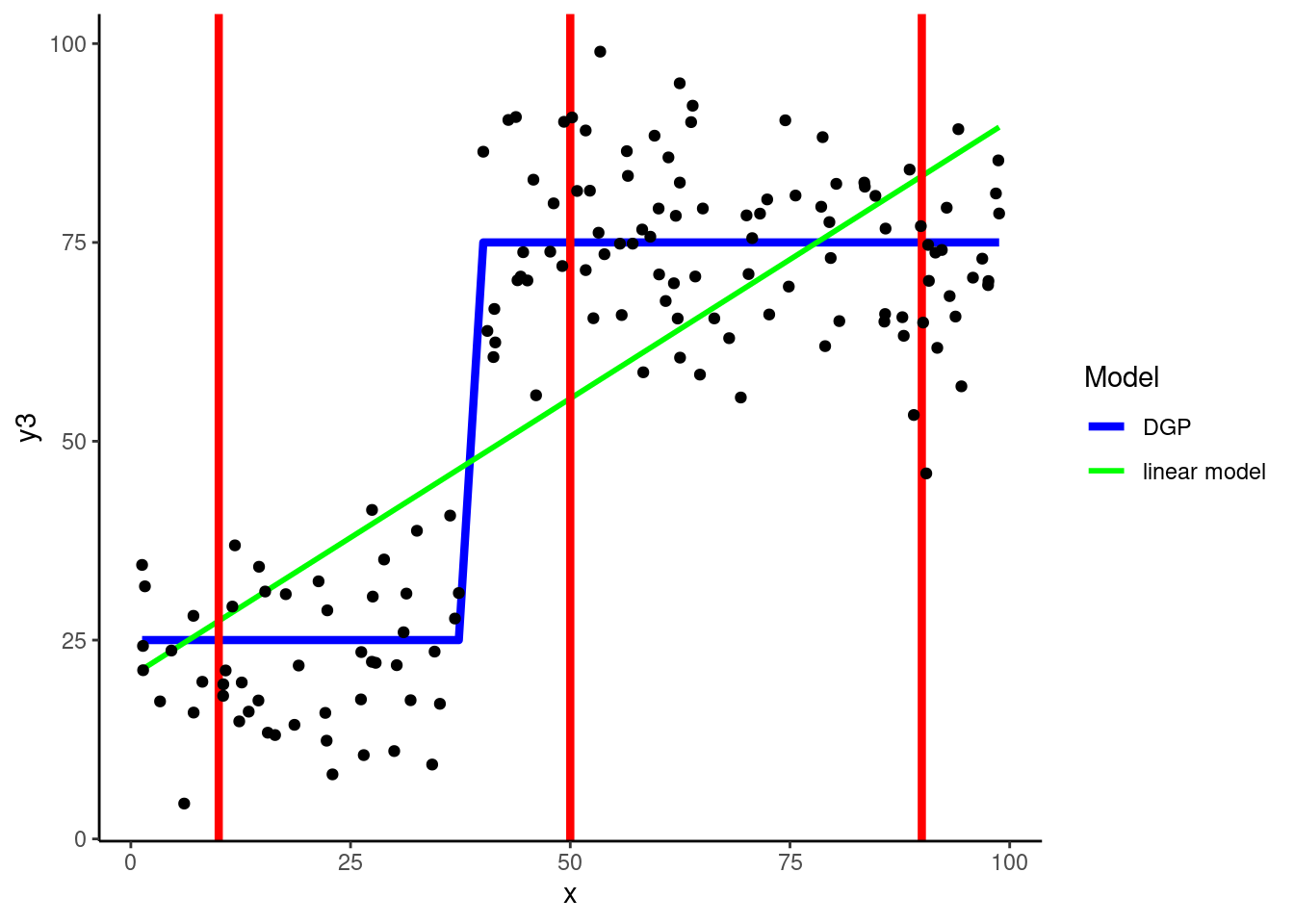

DGP: \(y3 = if\_else(x < 40, rnorm(150, 25, 10), rnorm(150, 75, 10))\)

KNN is our first example of a statistical algorithm that includes a hyperparameter, in this case \(k\)

Algorithm hyperparameters differ from parameters in that they cannot be estimated while fitting the algorithm to the training set

They must be set in advance

k = 5 is the default for kknn(), the engine from the kknn package that we will use to fit a KNN within tidymodels.

Using the polynomial DGP above, let’s look at a 5-NN yields

?kknn::train.kknn).nearest_neighbor() |>

set_engine("kknn") |>

set_mode("regression") |>

translate()K-Nearest Neighbor Model Specification (regression)

Computational engine: kknn

Model fit template:

kknn::train.kknn(formula = missing_arg(), data = missing_arg(),

ks = min_rows(5, data, 5))rec <-

recipe(y2 ~ x, data = data_trn_demo)

rec_prep <- rec |>

prep(data_trn_demo)

feat_trn_demo <- rec_prep |>

bake(NULL)fit_5nn_demo <-

nearest_neighbor() |>

set_engine("kknn") |>

set_mode("regression") |>

fit(y2 ~ ., data = feat_trn_demo)feat_val_demo <- rec_prep |>

bake(data_val_demo)Display 5NN predictions in validation

k = 5) does a pretty good job of representing the shape of the DGP (low bias)

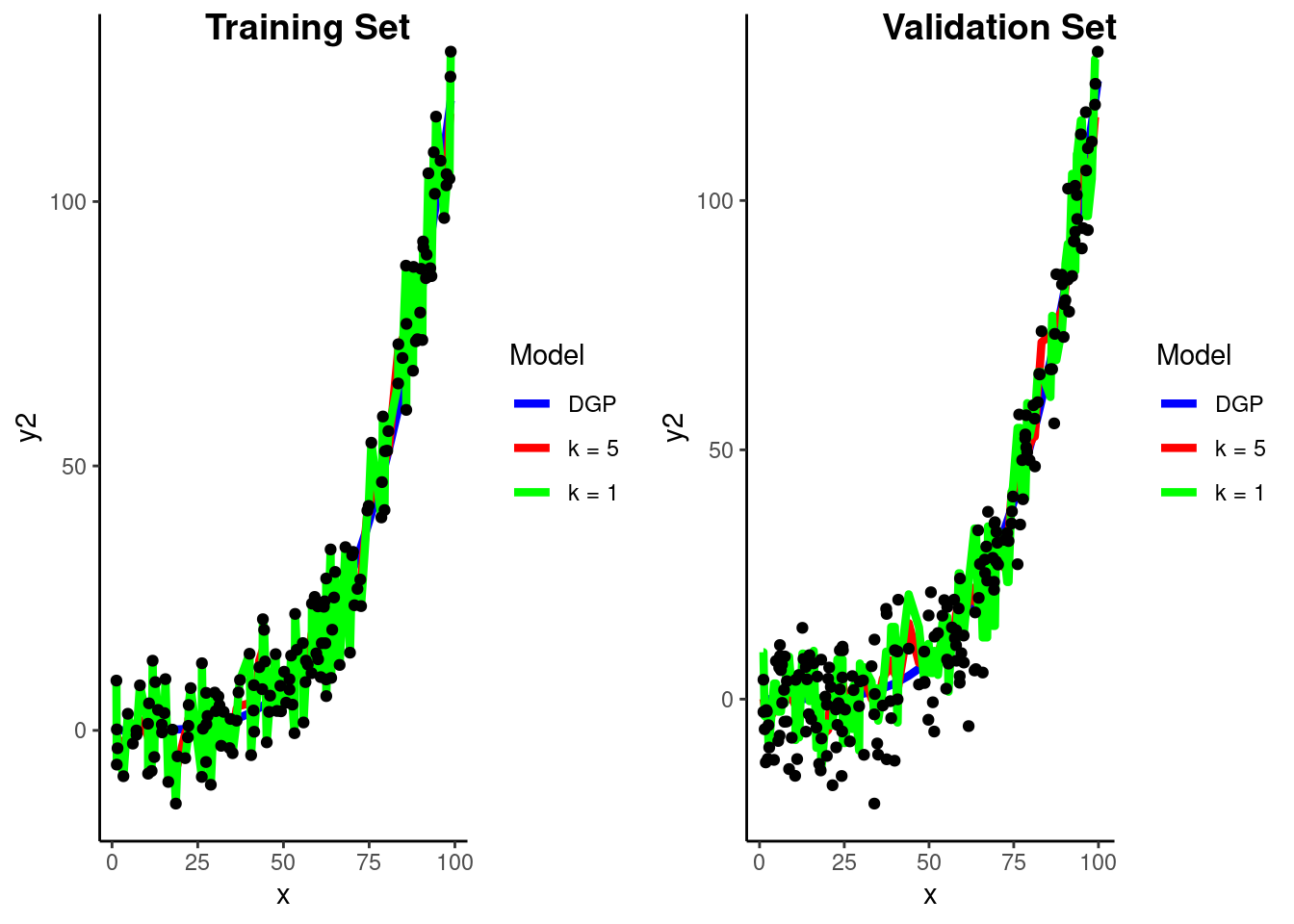

Let’s pause and consider our conceptual understanding of the impact of \(k\) on the bias-variance trade-off

k = 1

Fit new model

Recipe and features have not changed

fit_1nn_demo <-

1 nearest_neighbor(neighbors = 1) |>

set_engine("kknn") |>

set_mode("regression") |>

fit(y2 ~ ., data = feat_trn_demo)neighbors =

Visualize prediction models in Train and Validation

Calculate RMSE in validation for two KNN models

k = 1

rmse_vec(feat_val_demo$y2,

predict(fit_1nn_demo, feat_val_demo)$.pred)[1] 10.91586k = 5

rmse_vec(feat_val_demo$y2,

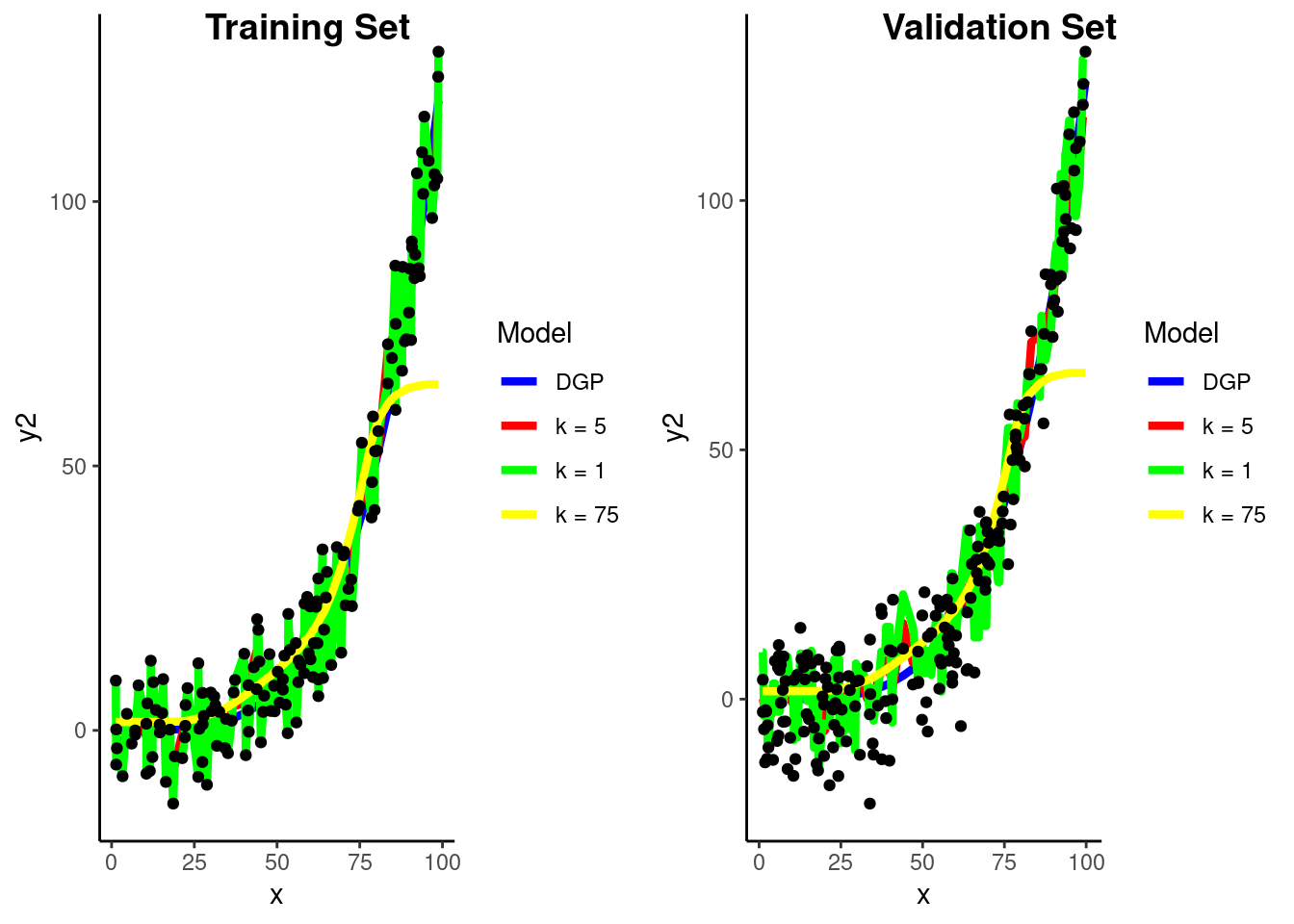

predict(fit_5nn_demo, feat_val_demo)$.pred)[1] 8.387035What if we go the other way and increase \(k\) to 75

fit_75nn_demo <-

nearest_neighbor(neighbors = 75) |>

set_engine("kknn") |>

set_mode("regression") |>

fit(y2 ~ ., data = feat_trn_demo)Visualize prediction models in Train and Validation

Calculate RMSE in validation for three KNN models

This is the bias-variance trade-off in action

k = 1 - high variancermse_vec(feat_val_demo$y2,

predict(fit_1nn_demo, feat_val_demo)$.pred)[1] 10.91586k = 5 - just right (well better at least)rmse_vec(feat_val_demo$y2,

predict(fit_5nn_demo, feat_val_demo)$.pred)[1] 8.387035k = 75 - high biasrmse_vec(feat_val_demo$y2,

predict(fit_75nn_demo, feat_val_demo)$.pred)[1] 15.34998To make a prediction for some new observation, we need to identify the observations from the training set that are nearest to it

Need a distance measure to define “nearest”

IMPORTANT: We care only about:

There are a number of different distance measures available (e.g., Euclidean, Manhattan, Chebyshev, Cosine, Minkowski)

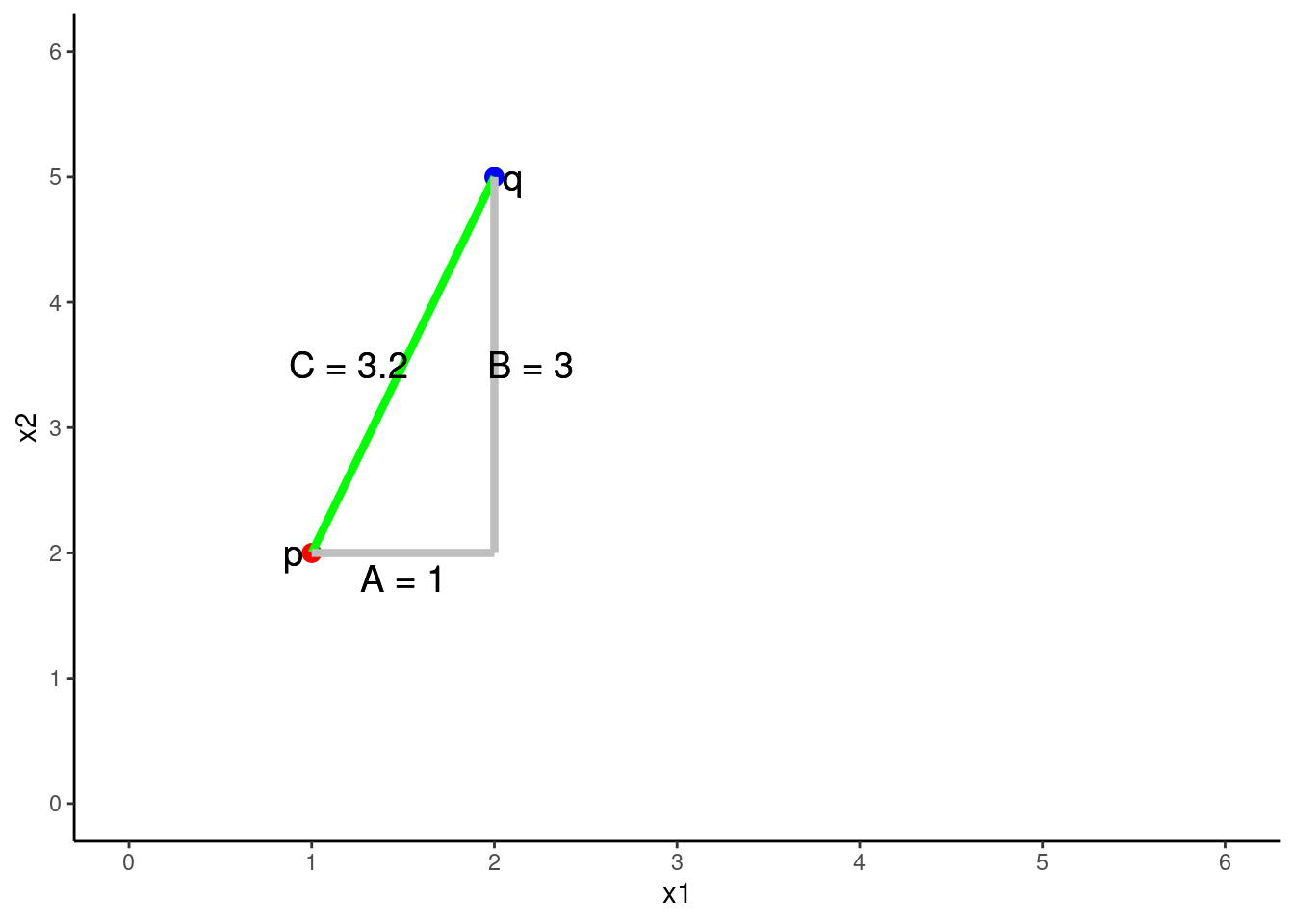

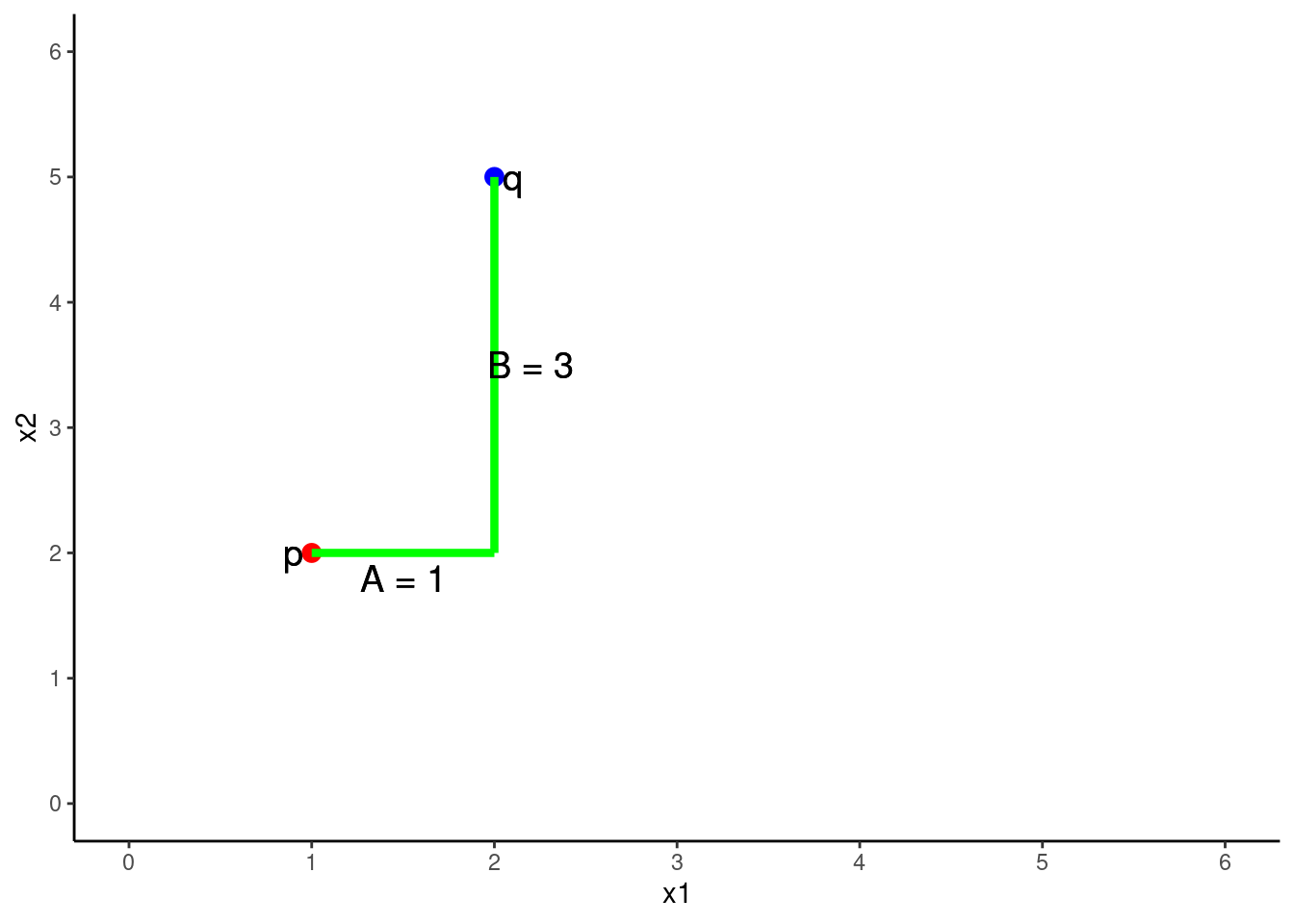

Euclidean distance between any two points is an n-dimensional extension of the Pythagorean formula (which applies explicitly with 2 features/2 dimensional space).

\(C^2 = A^2 + B^2\)

\(C = \sqrt{A^2 + B^2}\)

…where C is the distance between two points

The Euclidean distance between 2 points (p and q) in two dimensions (2 predictors, x1 = A, x2 = B)

\(Distance = \sqrt{A^2 + B^2}\)

\(Distance = \sqrt{(q1 - p1)^2 + (q2 - p2)^2}\)

\(Distance = \sqrt{(2 - 1)^2 + (5 - 2)^2}\)

\(Distance = 3.2\)

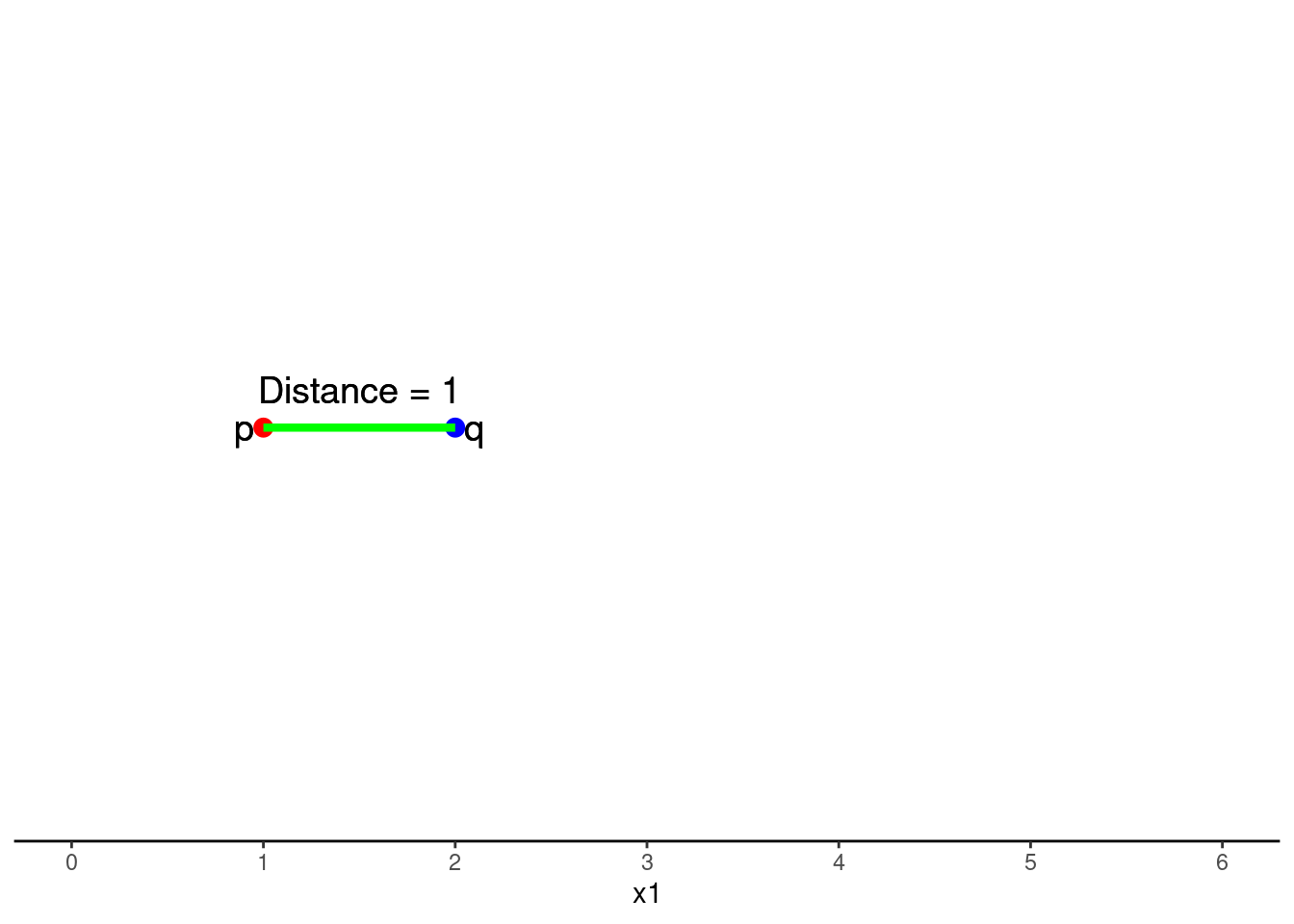

One dimensional (one feature) is simply the subtraction of scores on that feature (x1) between p and q

\(Distance = \sqrt{(q1 - p1)^2}\)

\(Distance = \sqrt{(2 - 1)^2}\)

\(Distance = 1\)

N-dimensional generalization for n features:

\(Distance = \sqrt{(q1 - p1)^2 + (q2 - p2)^2 + ... + (qn - pn)^2}\)

Manhattan distance is also referred to as city block distance

For two features/dimensions

\(Distance = |A + B|\)

kknn() uses Minkowski distance (see Wikipedia or less mathematical description)

p, referred to as distance in kknn()p = 2 and 1, respectivelynearest_neighbor()Distance is dependent on scales of all the features. We need to put all features on the same scale

step_scale(all_numeric_predictors()))step_range(all_numeric_predictors()))KNN requires numeric features (for distance calculation).

step_dummy(all_nominal_predictors())Let’s use KNN with Ames

overall_qual as numerick = 5 algorithmrec <-

recipe(sale_price ~ gr_liv_area + lot_area + year_built + garage_cars + overall_qual,

data = data_trn) |>

step_impute_median(garage_cars) |>

step_mutate(overall_qual = as.numeric(overall_qual)) |>

1 step_scale(all_numeric_predictors())?has_role for more details

rec_prep <- rec |>

prep(data_trn)

feat_trn <- rec_prep |>

bake(NULL)

feat_val <- rec_prep |>

bake(data_val)feat_trn |> skim_all()| Name | feat_trn |

| Number of rows | 1465 |

| Number of columns | 6 |

| _______________________ | |

| Column type frequency: | |

| numeric | 6 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 2.95 | 1.00 | 0.86 | 2.21 | 2.84e+00 | 3.44 | 11.03 | 1.43 | 5.19 |

| lot_area | 0 | 1 | 1.24 | 1.00 | 0.18 | 0.92 | 1.15e+00 | 1.39 | 20.14 | 11.20 | 182.91 |

| year_built | 0 | 1 | 66.48 | 1.00 | 63.40 | 65.86 | 6.65e+01 | 67.45 | 67.79 | -0.54 | -0.62 |

| garage_cars | 0 | 1 | 2.33 | 1.00 | 0.00 | 1.31 | 2.62e+00 | 2.62 | 5.23 | -0.26 | 0.10 |

| overall_qual | 0 | 1 | 4.30 | 1.00 | 0.71 | 3.54 | 4.24e+00 | 4.95 | 7.07 | 0.20 | -0.03 |

| sale_price | 0 | 1 | 180696.15 | 78836.41 | 12789.00 | 129500.00 | 1.60e+05 | 213500.00 | 745000.00 | 1.64 | 4.60 |

feat_val |> skim_all()| Name | feat_val |

| Number of rows | 490 |

| Number of columns | 6 |

| _______________________ | |

| Column type frequency: | |

| numeric | 6 |

| ________________________ | |

| Group variables | None |

Variable type: numeric

| skim_variable | n_missing | complete_rate | mean | sd | p0 | p25 | p50 | p75 | p100 | skew | kurtosis |

|---|---|---|---|---|---|---|---|---|---|---|---|

| gr_liv_area | 0 | 1 | 2.92 | 0.95 | 0.94 | 2.24 | 2.81 | 3.38 | 7.05 | 0.92 | 1.16 |

| lot_area | 0 | 1 | 1.28 | 1.27 | 0.21 | 0.92 | 1.17 | 1.44 | 26.32 | 15.64 | 301.66 |

| year_built | 0 | 1 | 66.47 | 1.04 | 63.23 | 65.90 | 66.61 | 67.45 | 67.79 | -0.66 | -0.41 |

| garage_cars | 0 | 1 | 2.27 | 0.99 | 0.00 | 1.31 | 2.62 | 2.62 | 5.23 | -0.24 | 0.22 |

| overall_qual | 0 | 1 | 4.28 | 0.98 | 0.71 | 3.54 | 4.24 | 4.95 | 7.07 | 0.00 | 0.35 |

| sale_price | 0 | 1 | 178512.82 | 75493.59 | 35311.00 | 129125.00 | 160000.00 | 213000.00 | 556581.00 | 1.42 | 2.97 |

fit_5nn_5num <-

nearest_neighbor() |>

set_engine("kknn") |>

set_mode("regression") |>

fit(sale_price ~ ., data = feat_trn)error_val <- bind_rows(error_val,

tibble(model = "5 numeric predictor 5nn",

rmse_val = rmse_vec(feat_val$sale_price,

predict(fit_5nn_5num, feat_val)$.pred)))

error_val# A tibble: 8 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.

5 7 feature linear model 34080.

6 8 feature linear model w/interaction 32720.

7 10 feature linear model w/interactions 32708.

8 5 numeric predictor 5nn 32837.KNN also mostly solved the linearity problem

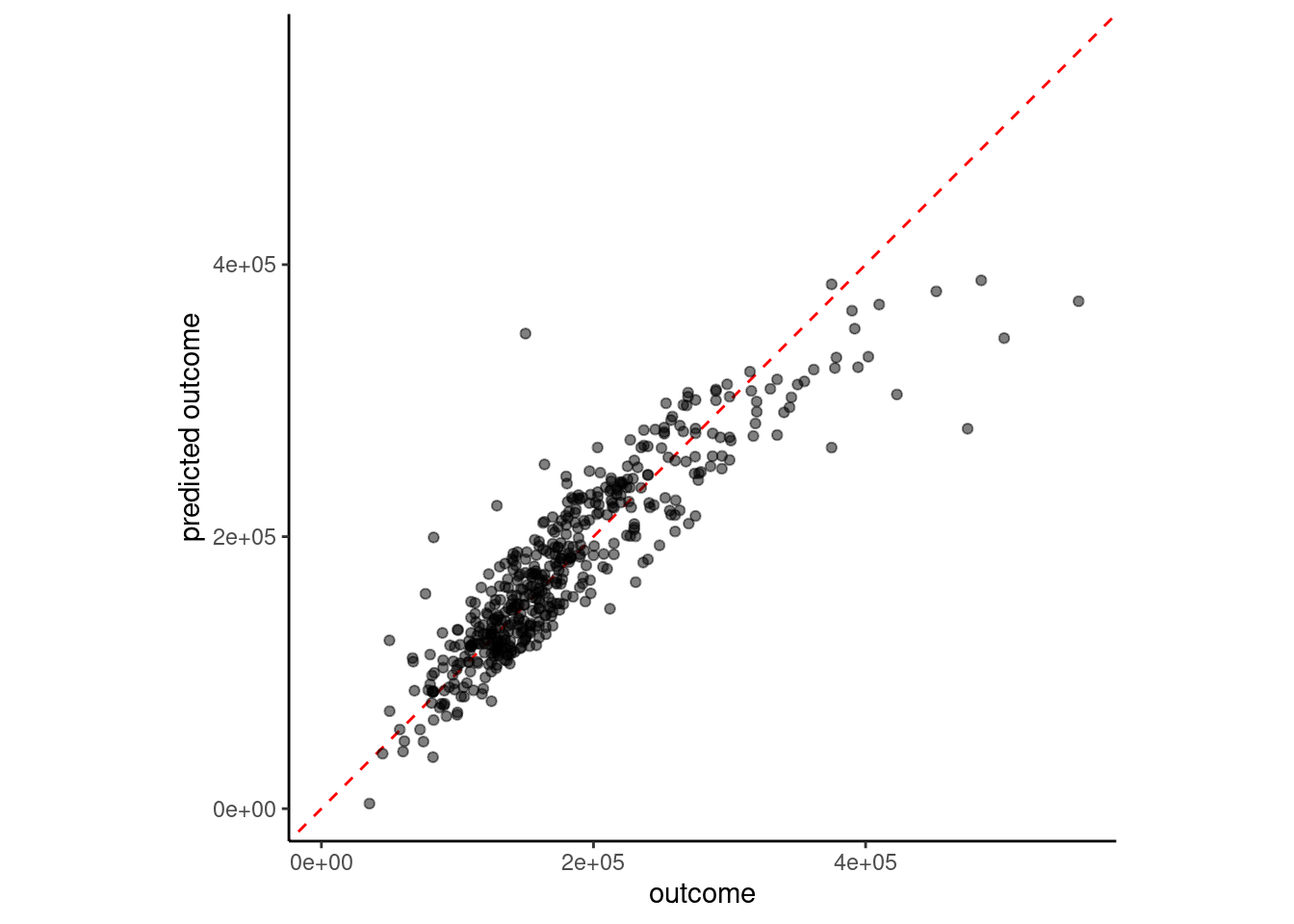

plot_truth(truth = feat_val$sale_price,

estimate = predict(fit_5nn_5num, feat_val)$.pred)

But 5NN may be overfit. k = 5 is pretty low

Again with k = 20

fit_20nn_5num <-

nearest_neighbor(neighbors = 20) |>

set_engine("kknn") |>

set_mode("regression") |>

fit(sale_price ~ ., data = feat_trn)# A tibble: 9 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.

5 7 feature linear model 34080.

6 8 feature linear model w/interaction 32720.

7 10 feature linear model w/interactions 32708.

8 5 numeric predictor 5nn 32837.

9 5 numeric predictor 20nn 30535.One more time with k = 50 to see where we are in the bias-variance function

fit_50nn_5num <-

nearest_neighbor(neighbors = 50) |>

set_engine("kknn") |>

set_mode("regression") |>

fit(sale_price ~ ., data = feat_trn)# A tibble: 10 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.

5 7 feature linear model 34080.

6 8 feature linear model w/interaction 32720.

7 10 feature linear model w/interactions 32708.

8 5 numeric predictor 5nn 32837.

9 5 numeric predictor 20nn 30535.

10 5 numeric predictor 50nn 31055.To better understand bias-variance trade-off, let’s look at error across these three values of \(k\) in train and validation for Ames

Training

k = 1rmse_vec(feat_trn$sale_price,

predict(fit_5nn_5num, feat_trn)$.pred)[1] 19012.94rmse_vec(feat_trn$sale_price,

predict(fit_20nn_5num, feat_trn)$.pred)[1] 27662.2rmse_vec(feat_trn$sale_price,

predict(fit_50nn_5num, feat_trn)$.pred)[1] 31069.12Validation

k = 1)k = 20 relative to 5 and 1rmse_vec(feat_val$sale_price,

predict(fit_5nn_5num, feat_val)$.pred)[1] 32837.37rmse_vec(feat_val$sale_price,

predict(fit_20nn_5num, feat_val)$.pred)[1] 30535.04rmse_vec(feat_val$sale_price,

predict(fit_50nn_5num, feat_val)$.pred)[1] 31054.6Let’s do one final example and add one of our nominal variables into the model: ms_zoning

rec <-

recipe(sale_price ~ gr_liv_area + lot_area + year_built + garage_cars +

overall_qual + ms_zoning, data = data_trn) |>

step_impute_median(garage_cars) |>

step_mutate(overall_qual = as.numeric(overall_qual)) |>

step_mutate(ms_zoning = fct_collapse(ms_zoning,

"residential" = c("res_high", "res_med", "res_low"),

"commercial" = c("agri", "commer", "indus"),

"floating" = "float")) |>

step_dummy(ms_zoning) |>

step_scale(all_numeric_predictors())rec_prep <- rec |>

prep(data_trn)

feat_trn <- rec_prep |>

bake(NULL)

feat_val <- rec_prep |>

bake(data_val)fit_20nn_5num_mszone <-

nearest_neighbor(neighbors = 20) |>

set_engine("kknn") |>

set_mode("regression") |>

fit(sale_price ~ ., data = feat_trn)# A tibble: 11 × 2

model rmse_val

<chr> <dbl>

1 simple linear model 51375.

2 4 feature linear model 39903.

3 4 feature linear model with YJ 41660.

4 6 feature linear model w/ms_zoning 39846.

5 7 feature linear model 34080.

6 8 feature linear model w/interaction 32720.

7 10 feature linear model w/interactions 32708.

8 5 numeric predictor 5nn 32837.

9 5 numeric predictor 20nn 30535.

10 5 numeric predictor 50nn 31055.

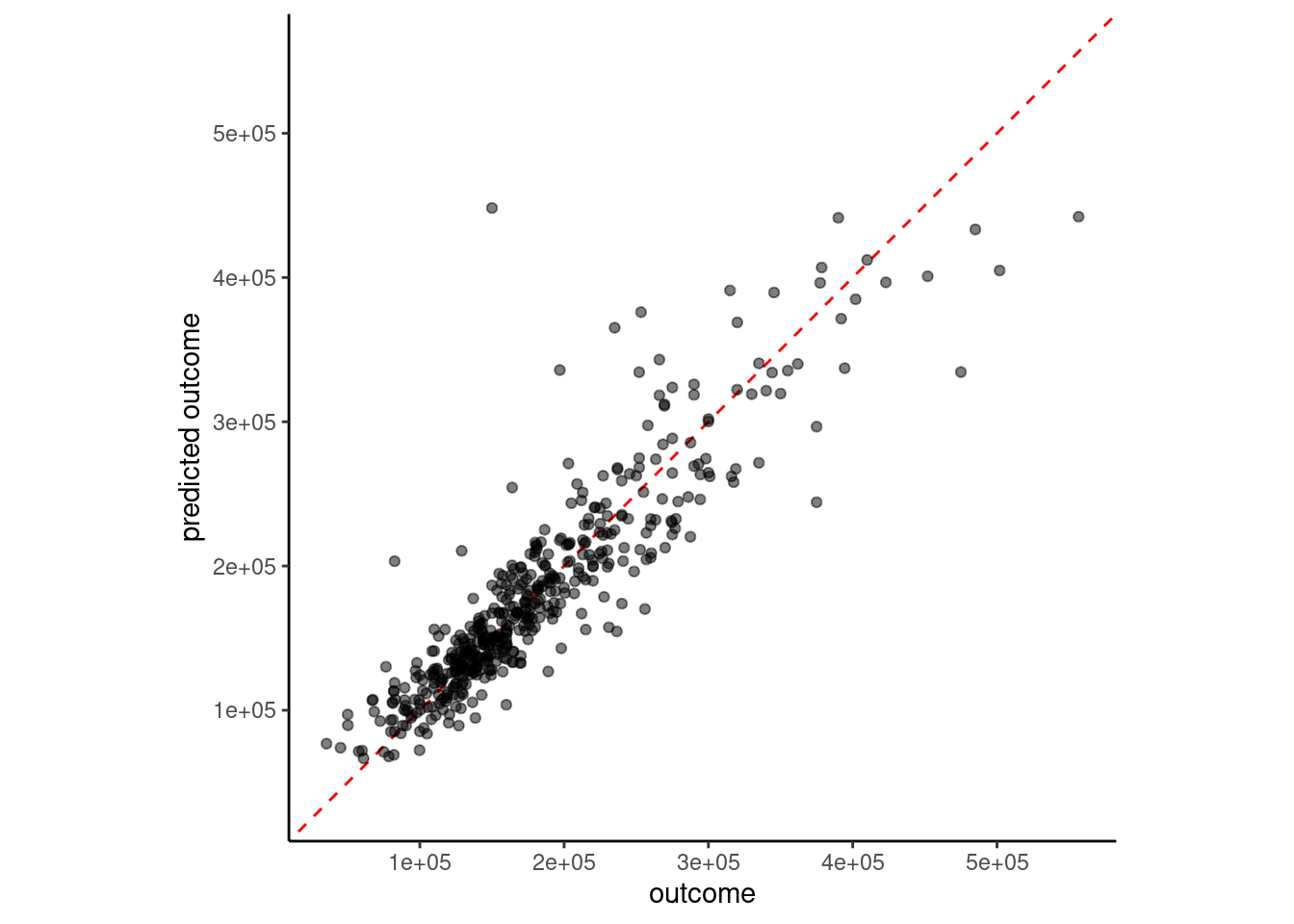

11 5 numeric predictor 20nn with ms_zoning 30172.As a teaser, here is another performance metric for this model - \(R^2\). Not too shabby! Remember, there is certainly some irreducible error in sale_price that will put a ceiling on \(R^2\) and a floor on RMSE

rsq_vec(feat_val$sale_price,

predict(fit_20nn_5num_mszone, feat_val)$.pred)[1] 0.8404044Overall, we now have a model that predicts housing prices with about 30K of RMSE and accounting for 84% of the variance. I am sure you can improve on this!

read_csv(here::here(path_data, "lunch_003.csv")) |>

print_kbl()Rows: 20 Columns: 2

── Column specification ────────────────────────────────────────────────────────

Delimiter: ","

chr (1): name

dbl (1): rmse_test

ℹ Use `spec()` to retrieve the full column specification for this data.

ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.| name | rmse_test |

|---|---|

| Dong | 25495.53 |

| Simental | 28733.22 |

| Phipps | 28794.84 |

| Yang | 30420.01 |

| Li | 31534.42 |

| Yu | 31874.12 |

| NA | 32606.15 |

| NA | 33614.59 |

| NA | 33877.07 |

| NA | 33879.19 |

| NA | 34315.31 |

| NA | 34692.22 |

| NA | 35034.74 |

| NA | 35154.67 |

| NA | 35683.85 |

| NA | 36101.95 |

| NA | 36266.80 |

| NA | 36473.84 |

| NA | 38974.43 |

| NA | 42367.31 |

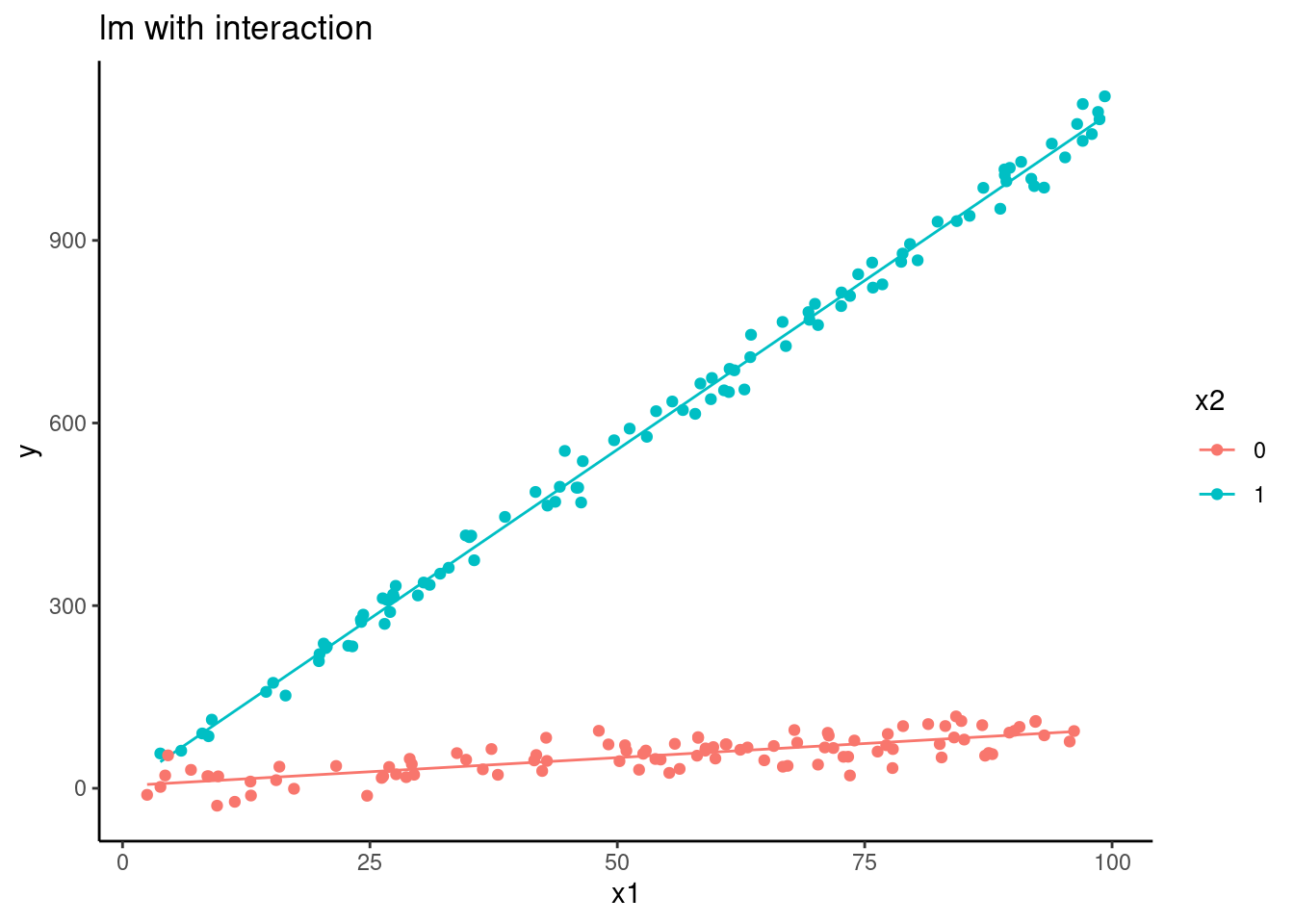

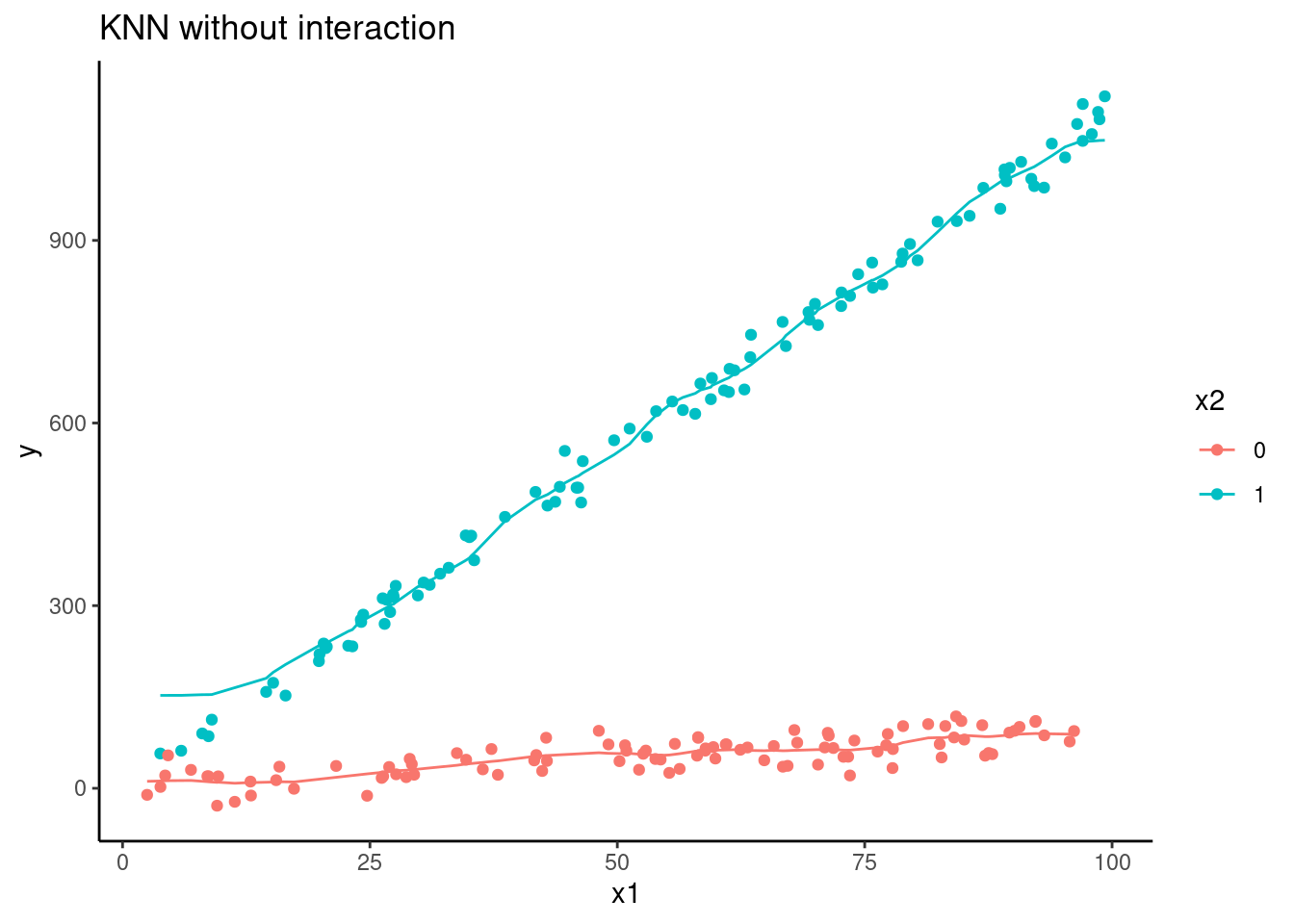

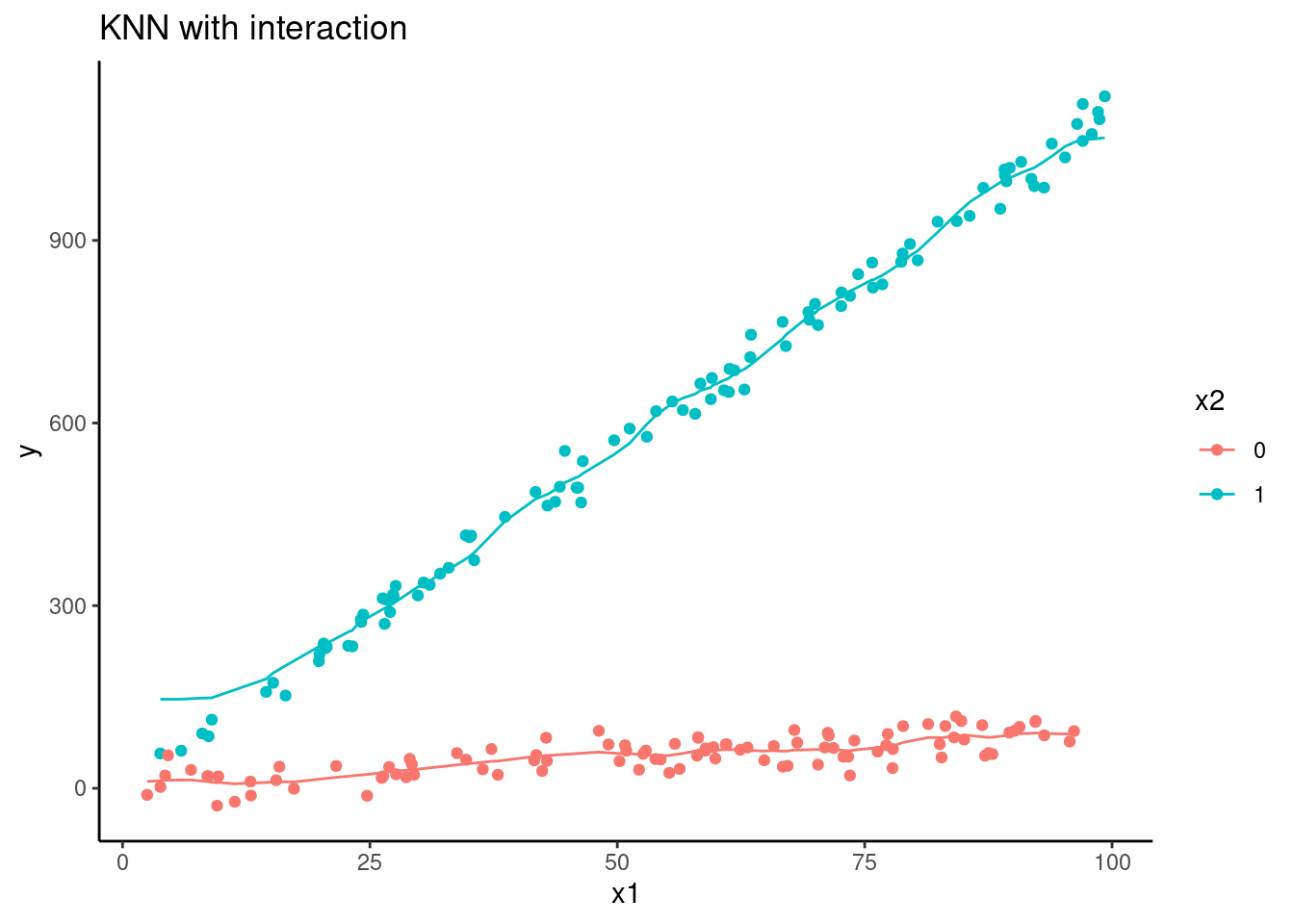

n <- 200

set.seed(5433)

d <- tibble(x1 = runif(n, 0,100), # uniform

x2 = rep(c(0,1), n/2), # dichotomous

x1_x2 = x1*x2, # interaction

y = rnorm(n, 0 + 1*x1 + 10*x2 + 10* x1_x2, 20)) #DGP + noise

fit_lm <-

linear_reg() |>

set_engine("lm") |>

fit(y ~ x1 + x2, data = d)

fit_lm_int <-

linear_reg() |>

set_engine("lm") |>

fit(y ~ x1 + x2 + x1_x2, data = d)

fit_knn <-

nearest_neighbor(neighbors = 20) |>

set_engine("kknn") |>

set_mode("regression") |>

fit(y ~ x1 + x2, data = d)

fit_knn_int <-

nearest_neighbor(neighbors = 20) |>

set_engine("kknn") |>

set_mode("regression") |>

fit(y ~ x1 + x2 + x1_x2, data = d)

d <- d |>

mutate(pred_lm = predict(fit_lm, d)$.pred,

pred_lm_int = predict(fit_lm_int, d)$.pred,

pred_knn = predict(fit_knn, d)$.pred,

pred_knn_int = predict(fit_knn_int, d)$.pred)d |>

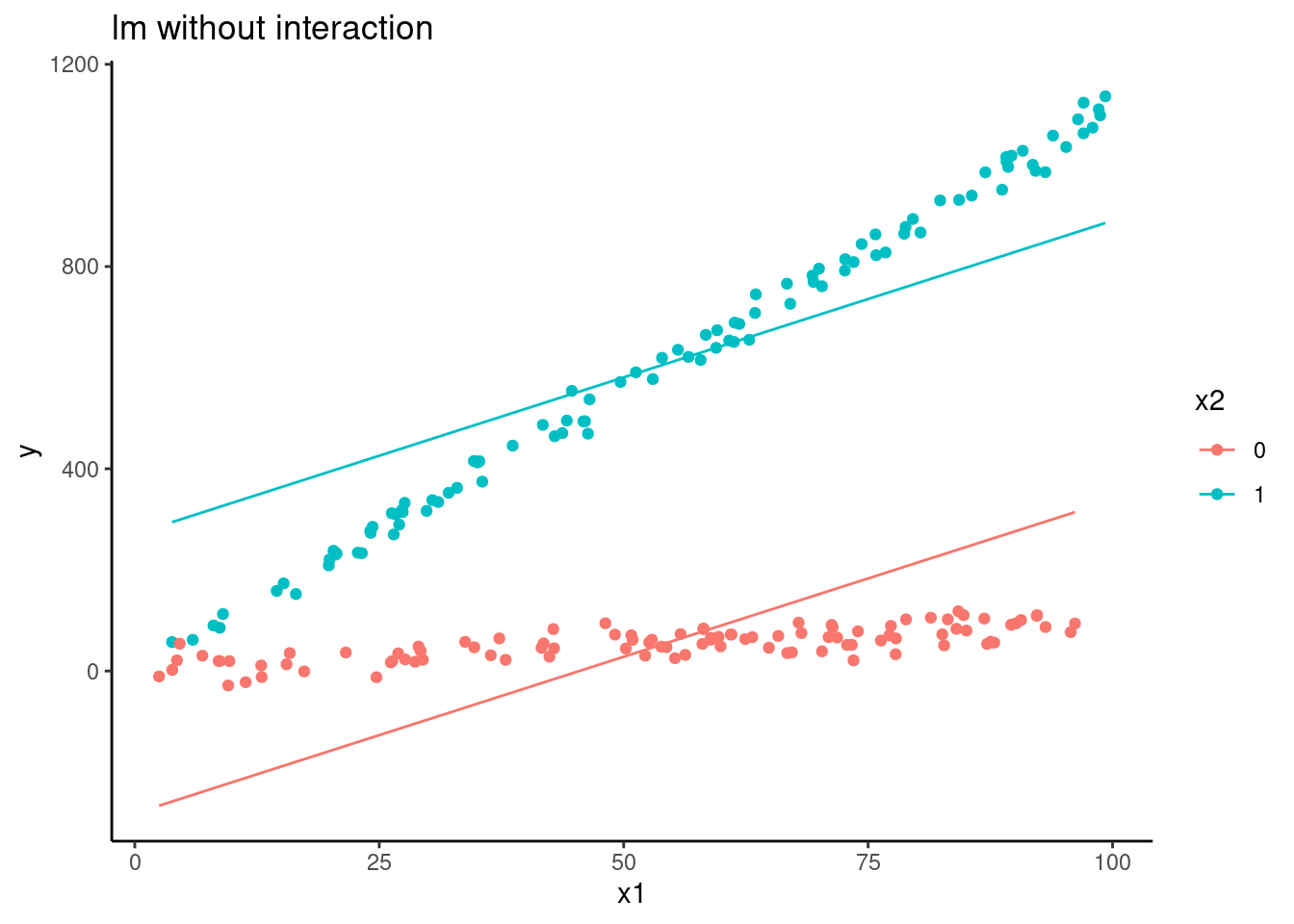

ggplot(aes(x = x1, group = factor(x2), color = factor(x2))) +

geom_line(aes(y = pred_lm)) +

geom_point(aes(y = y)) +

ggtitle("lm without interaction") +

ylab("y") +

scale_color_discrete(name = "x2")

d |>

ggplot(aes(x = x1, group = factor(x2), color = factor(x2))) +

geom_line(aes(y = pred_lm_int)) +

geom_point(aes(y = y)) +

ggtitle("lm with interaction") +

ylab("y") +

scale_color_discrete(name = "x2")

d |>

ggplot(aes(x = x1, group = factor(x2), color = factor(x2))) +

geom_line(aes(y = pred_knn)) +

geom_point(aes(y = y)) +

ggtitle("KNN without interaction") +

ylab("y") +

scale_color_discrete(name = "x2")

d |>

ggplot(aes(x = x1, group = factor(x2), color = factor(x2))) +

geom_line(aes(y = pred_knn_int)) +

geom_point(aes(y = y)) +

ggtitle("KNN with interaction") +

ylab("y") +

scale_color_discrete(name = "x2")

Use of plot_truth() [predicted vs. observed]

Residuals do not have mean of 0 for every \(\hat{y}\)

Non-normal residuals

Heteroscasticity

Transformation of outcome?